WEEKLY FINANCIAL MARKET REPORT AS OF 11TH OCTOBER 2024

KEY INSIGHTS

Ghana and IMF reach Staff Level Agreement after 3rd PC-PEG Review (Ministry of Finance, 2024)

The Bank of Ghana set Bulk Distribution Forward Rates at GHS15.8682 per dollar, with a target amount of $20 million.

This week, trading on the local stock market slowed dramatically, with only 1,114,611 shares changing hands—a steep 75.98% plunge from the robust 4.6 million shares traded last week.

Rains in Ivory Coast have severely impacted cocoa production and transportation, with only 12,960 metric tons (MT) of cocoa beans shipped from October 1 to October 6, a sharp decline from 50,138 metric tons during the same period last year.

BDC FORWARD RATE

The Bank of Ghana held a Forex Forward Rates Auction (No. 0062/2024/019) on October 10, 2024, specifically for Bulk Distribution Companies (BDCs), targeting a 30-day tenor. Ten bids were submitted by banks, with the proposed exchange rates ranging from 15.7000 to 15.8800 GHS/USD. The Bank of Ghana set the official forward rate at 15.8682 GHS/USD, aiming to meet a target amount of $20 million. This helps manage foreign exchange availability for BDCs, aiding currency stability and short-term liquidity.

PRIMARY DEBT MARKET ISSUANCE WEEK

The Government of Ghana Treasury Bill rates experienced a divergent movement across all maturities compared to the previous week. This week saw total bids of GH₵ 3,887.83 million for the 91-day bill, GH₵ 500.68 million for the 182-day bill, and GH₵ 225.42 million for the 364-day bill, all of which were fully accepted.

The 91-day bill had bid rates ranging from 25.4527% to 25.800%, with a weighted average rate of 25.4568%. For the 182-day bill, rates ranged between 26.7959% and 27.0001%, averaging 26.9045%. The 364-day bill recorded bid rates from 28.5017% to 28.7001%, with a weighted average rate of 28.5814%.

| Security | Current Wk % | Previous Wk % |

| 91-Day GoG Bill | 25.6182 | 25.4568 |

| 182-Day GoG Bill | 26.9045 | 26.8001 |

| 364-Day GoG Bill | 28.5814 | 28.5174 |

Source(s): Bank of Ghana

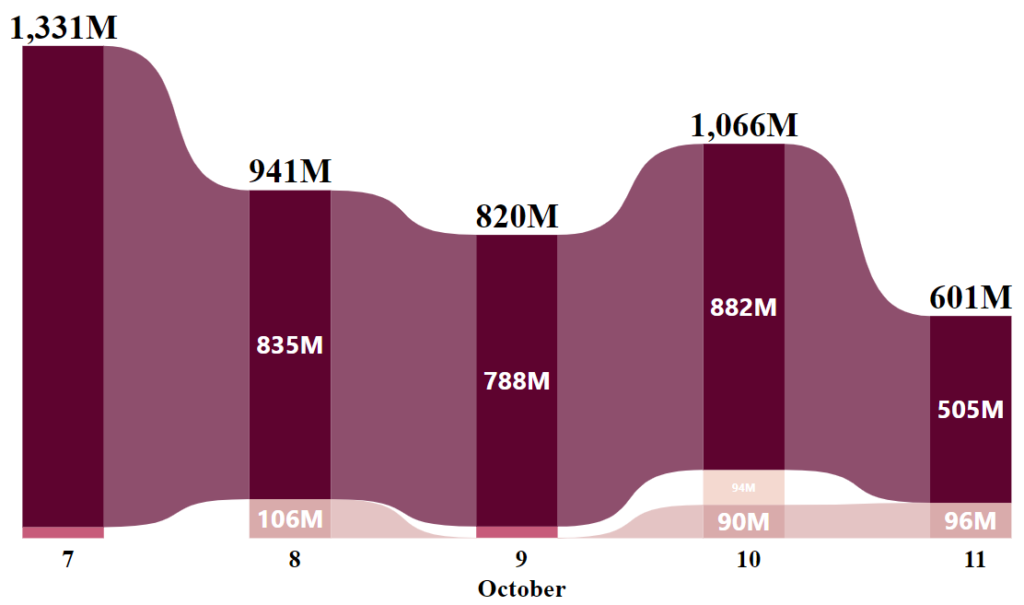

GHANA FIXED INCOME MARKET VOLUME TRADED

The Ghana Fixed Income Market closed the week with a total volume traded of GH₵ 4.76 billion. A total of 8,623 trades were made of which 99.44% were Treasury bills, and 0.27% were Sell/Buy Back Trades.

Week’s Ghana Fixed Income Market Total Volume Traded

Trading activity on the Ghana Fixed Income Market (GFIM) for the week of October 7 to October 11, 2024, showed fluctuating volumes across various security types. The week commenced with a trading volume of GH₵ 1,331 million on October 7, primarily driven by Treasury Bills. This figure dipped to GH₵ 941 million on October 8, with the largest contribution attributed to Treasury Bills and Sell/Buy Back Trades.

The downward momentum persisted on October 9, again with contributions largely attributed to Treasury Bills. On October 10, trading volumes surged to GH₵ 1,066 million, led by Treasury Bills. The week concluded with a significant decline to GH₵ 601 million on October 11, driven by strong contributions from Treasury Bills and Sell/Buy Back Trades. Treasury Bills consistently dominated market activity throughout the week.

EQUITY MARKET

Trading activity on the local bourse declined this week, with a volume of 1,114,611 shares exchanged, marking a 75.98% decrease from the 4,640,938 shares posted last week. The total traded value also saw significant upswing of 31.47%, reaching GH₵ 14.33 million. This, however, resulted in a 0.24% dip in the market capitalization, closing at GH₵ 98.94 billion.

Week’s Equities Top Gainers & Laggards

In terms of market indices, the GSE Composite Index (GSE-CI) closed at 4,346.70, showing a weekly loss of 0.42% and a monthly loss of 0.35%, but maintaining a strong year-to-date gain of 38.86%. Meanwhile, the GSE Financial Stocks Index (GSE-FSI) also increased to reach 2,203.38 points, posting a slight weekly increase of 0.2%, a monthly rise of 4.07%, and a year-to-date gain of 15.87%.

| EQUITY MARKET MOST TRADED STOCKS | ||

| Ticker | Traded Volume | Price (GHS) |

| MTNGH | 455,586 | 2.15 |

| GCB | 297,255 | 6.15 |

| SIC | 134,099 | 0.25 |

| ACCESS | 73,851 | 4.32 |

| CAL | 73,269 | 0.28 |

Source(s): Ghana Stock Exchange

| TOP PERFORMING AFRICAN STOCK INDICES YEAR-TO-DATE | |||

| Country | Index | Level | YTD % |

| Zambia | LuSE ASI | 15,933.13 | ▲47.15 |

| Ghana | GSE-CI | 4,364.83 | ▲38.86 |

| Nigeria | NGSE ASI | 97,606.63 | ▲30.54 |

| Malawi | MSE ASI | 144,019.24 | ▲29.80 |

| Uganda | USE ASI | 1,121.38 | ▲28.52 |

Source(s): African Markets, AFX Kwayisi

COMMODITY MARKET

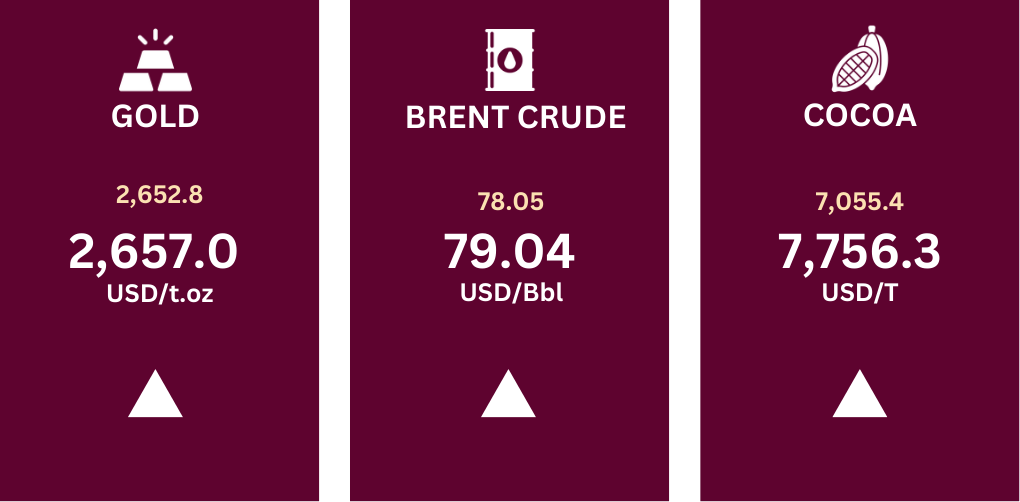

The commodities market experienced a divergent performance this week. Gold rose above $2,640 per ounce on Friday, extending gains from the previous session as traders continued to assess the Federal Reserve’s policy direction following mixed economic data. US headline inflation slowed less than expected in September, while underlying inflation rose more than forecast, halting recent progress toward moderating price pressures.

Brent crude oil futures lost 0.4% to settle at $79 on Friday as investors weighed the potential supply disruptions from the Middle East conflict and the effects of Hurricane Milton on fuel demand in Florida.

Source(s): Trading Economics

Cocoa futures have been steadily rising to trade near $7,800, their highest since late September, amid concerns over shrinking global supplies. Traders also noted some support from the situation in top grower Ivory Coast, where heavy rains are damaging roads, hampering the harvest and transportation of cocoa beans. From October 1 to October 6, farmers shipped only 12,960 MT to ports, down from 50,138 MT during the same period last year. Meanwhile, the current crop in Ghana, the world’s second-largest cocoa producer, appears promising.

CURRENCY MARKET

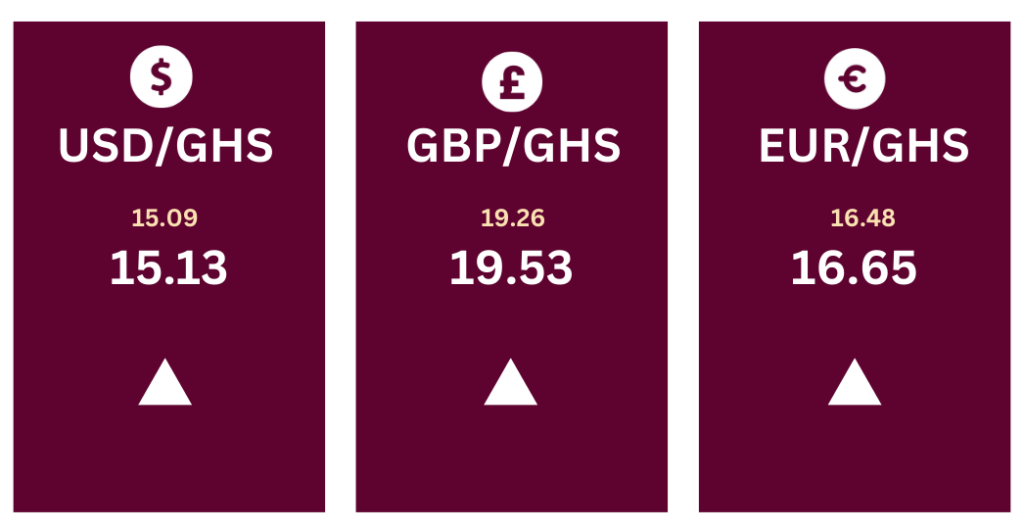

The Ghanaian cedi showed a varied performance against major currencies in recent exchange rate movements. The cedi depreciated slightly against the US dollar, with the USD/GHS pair rising from 15.79 to 15.90. Similarly, it saw a minor drop against the euro, as the EUR/GHS rate edged up from 17.30 to 17.40. In contrast, the cedi remained stable against the British pound, with the GBP/GHS rate holding steady at 20.79. This suggests mild pressure on the cedi, particularly against the dollar and euro, while maintaining stability against the pound.

Source(s): Bank of Ghana

Source(s): Bank of Ghana

Source(s): Bank of Ghana