WEEKLY FINANCIAL MARKET REPORT AS OF 4TH OCTOBER 2024

KEY INSIGHTS

Ghana’s inflation surged to 21.5% in September, reversing a six-month decline

Trading on the local bourse plummeted 98%, with only 4.6M shares exchanged this week.

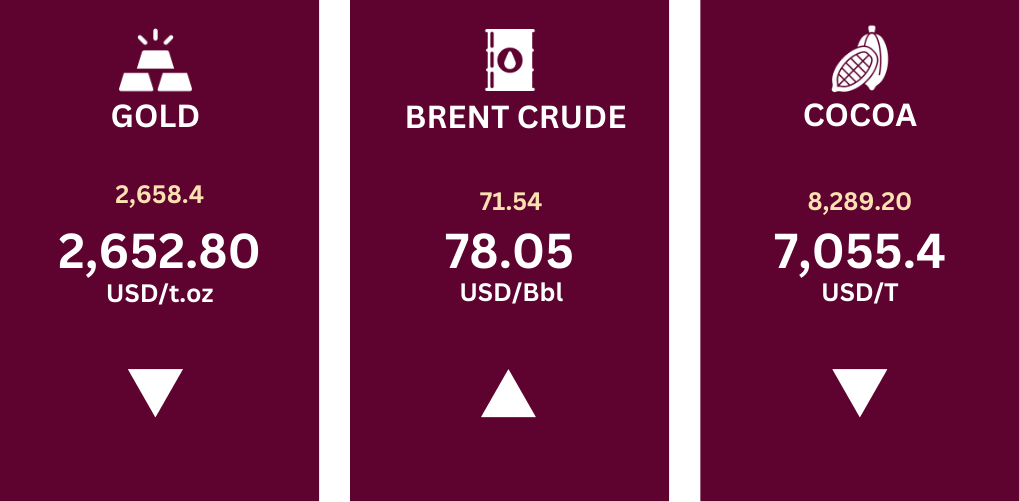

Brent crude hit a five-week high at $78.05 amid Middle East supply concerns.

Cocoa prices plunged to $7,055.40 per ton, the lowest since mid-March.

INFLATION RATE

Ghana’s annual consumer inflation rate increased to 21.5% in September 2024, up from 20.4% in August, reversing a six-month downward trend. The uptick was primarily driven by rising food prices, which surged to 22.1% from 19.1% the previous month. In contrast, non-food inflation eased slightly to 20.9% from 21.5%. On a month-on-month basis, consumer prices rose by 2.8% in September, following a 0.7% decline in August. This shift in inflation dynamics highlights renewed pressures, particularly in the food sector.

PRIMARY DEBT MARKET ISSUANCE WEEK

The Government of Ghana Treasury Bill rates experienced a general decline across all maturities compared to the previous week. This week saw total bids of GH₵ 2,911.51 million for the 91-day bill, GH₵ 572.95 million for the 182-day bill, and GH₵ 189.95 million for the 364-day bill, all of which were fully accepted.

The 91-day bill had bid rates ranging from 25.400% to 25.500%, with a weighted average rate of 25.4568%. For the 182-day bill, rates ranged between 26.7831% and 26.8017%, averaging 26.8001%. The 364-day bill recorded bid rates from 28.5017% to 28.5175%, with a weighted average rate of 28.5174%.

| Security | Current Wk % | Previous Wk % |

| 91-Day GoG Bill | 25.4568 | 25.6439 |

| 182-Day GoG Bill | 26.8001 | 26.9248 |

| 364-Day GoG Bill | 28.5174 | 28.6785 |

Source(s): Bank of Ghana

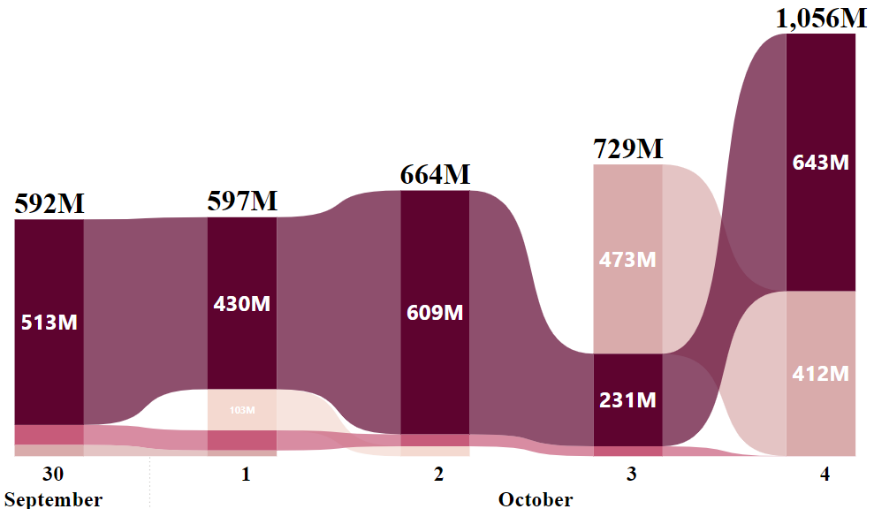

GHANA FIXED INCOME MARKET VOLUME TRADED

The Ghana Fixed Income Market closed the week with a total volume traded of GH₵ 3.64 billion. A total of 8,628 trades were made of which 99.56% were Treasury bills, and 0.19% were New GoG Notes & Bonds.

Week’s Ghana Fixed Income Market Total Volume Traded

Trading activity on the Ghana Fixed Income Market (GFIM) for the week of September 30 to October 4, 2024, showed fluctuating volumes across various security types. The week commenced with a trading volume of GH₵ 592 million on September 30, primarily driven by Treasury Bills. This figure increased to GH₵ 597 million on October 1, bolstered by continued interest in Treasury Bills and Corporate Bonds.

The upward momentum persisted on October 2, again largely due to Treasury Bills. On October 3, trading volumes surged to GH₵ 729 million, led by Sell/Buy Back Trades. The week concluded with a significant rise to GH₵ 1,056 million on October 4, driven by strong contributions from Treasury Bills and Sell/Buy Back Trades. Treasury Bills consistently dominated market activity throughout the week.

EQUITY MARKET

Trading activity on the local bourse declined this week, with a volume of 4,640,938 shares exchanged, marking a 98.25% decrease from the 266,695,648 shares posted last week. The total traded value also saw a significant dip of 97.92%, reaching GH₵ 10.92 million. This downturn in trading activity resulted in a 0.03% dip in the market capitalization, closing at GH₵ 99.20 billion.

Week’s Equities Top Gainers & Laggards

In terms of market indices, the GSE Composite Index (GSE-CI) closed at 4,364.83, showing a weekly loss of 0.35% and a monthly gain of 0.39%, but maintaining a strong year-to-date gain of 39.44%. Meanwhile, the GSE Financial Stocks Index (GSE-FSI) also increased to reach 2,198.88 points, posting a slight weekly increase of 0.39%, a monthly rise of 3.79%, and a year-to-date gain of 15.63%.

| EQUITY MARKET MOST TRADED STOCKS | ||

| Ticker |

Traded Volume |

Price (GHS) |

| MTNGH |

4,167,655 |

2.17 |

| ACCESS |

247,903 |

4.32 |

| EGL |

112,695 |

1.99 |

| CAL |

18,196 |

0.28 |

| GOIL |

16,978 |

1.50 |

Source(s): Ghana Stock Exchange

| TOP PERFORMING AFRICAN STOCK INDICES YEAR-TO-DATE | |||

| Country |

Index |

Level |

YTD % |

| Zambia |

LuSE ASI |

15,909.52 |

▲46.93 |

| Ghana |

GSE-CI |

4,364.83 |

▲39.44 |

| Nigeria |

NGSE ASI |

97,520.54 |

▲30.42 |

| Malawi |

MSE ASI |

143,705.95 |

▲29.52 |

| Uganda |

USE ASI |

1,103.13 |

▲26.43 |

Source(s): African Markets, AFX Kwayisi

COMMODITY MARKET

The commodities market experienced a divergent performance this week. Gold prices slightly dipped, decreasing from US$ 2,658.4 to US$ 2,652.80 per troy ounce. While gold has lacked the strong momentum it enjoyed for much of the last month, the yellow metal held considerable ground this week and may have consolidated a solid platform for the start of Q4.

In contrast, Brent crude prices slightly increased, moving from US$ 71.54 to US$ 78.05 per barrel, the highest level in five weeks, amid worries about potential supply disruption in the Middle East. Meanwhile, OPEC’s spare production capacity and the stability of global crude supplies eased supply fears.

Source(s): Trading Economics

Source(s): Trading Economics

Cocoa prices dipped, declining from US$ 8,289.20 to US$ 7,055.40 per ton, reaching their lowest since mid-March, as traders noted fund liquidation of long positions. Moreover, favorable weather in top growers Ivory Coast and Ghana is improving the main crop outlook and helping to keep a lid on cocoa prices after a strong rally earlier this year.

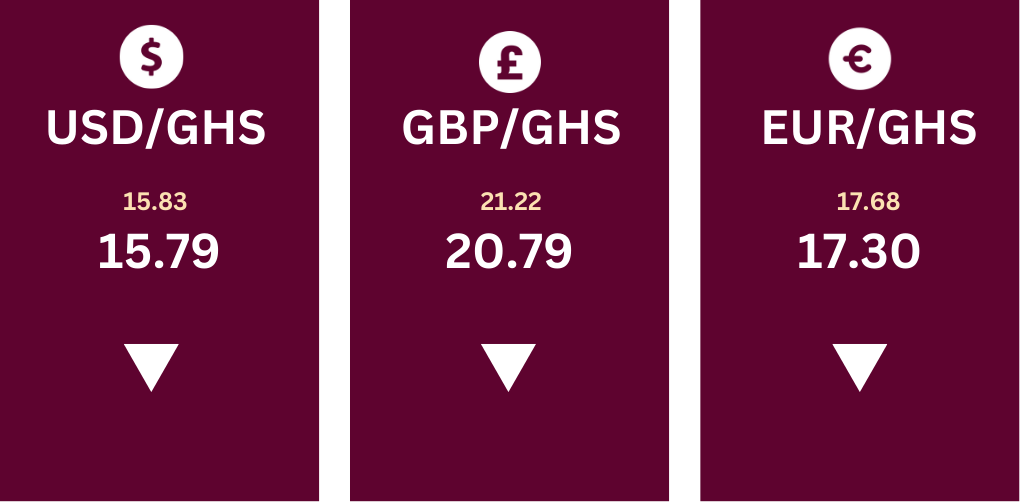

The Ghanaian cedi has demonstrated slight appreciation against major currencies, as reflected in recent exchange rate movements. The USD/GHS pair fell from 15.83 to 15.79, while the GBP/GHS dropped from 21.22 to 20.79, and the EUR/GHS declined from 17.68 to 17.30.

This consistent, albeit modest, strengthening of the cedi could signal improving market sentiment or the impact of recent monetary policy measures. However, further monitoring is necessary to determine whether this trend will persist in the face of broader macroeconomic pressures.

Source(s): Bank of Ghana

DISCLAIMER: The information contained in this weekly update on the financial markets is intended for informational purposes only and should not be construed as financial, investment or other professional advice. The data are derived from internal and external sources that FFC Research finds reliable. FFC Research assumes no responsibility or liability for any actions taken based on the information contained in this report.

Research Analyst – Cedric Asante | Email: cedric.asante@firstfinancecompany.com