WEEKLY FINANCIAL MARKET REPORT AS OF 25TH OCTOBER 2024

KEY HEADLINES & INSIGHTS

Climate Financing Division established in the Ministry of Finance. (Ministry of Finance, 2024)

National Insurance Commission working on creating an enabling environment to support market innovations and integration of technology into the industry’s operations (National Insurance Commission, 2024)

The Bank of Ghana’s eCedi pilot, a feasibility of a digital complement to physical currency, has achieved a major milestone, recording a transaction value of GH₵ 473 million, with over 96,000 transactions during the testing phase. (Bank of Ghana, 2024)

Ivory Coast’s bean arrivals reached 192,804 tons from October 1 to 20, up 12.9% from 170,794 tons during the same period last year, marking the first year-over-year increase.

PRIMARY DEBT MARKET ISSUANCE WEEK

The Government of Ghana Treasury Bill interest rates experienced marginal upswing across all tenors compared to the previous week as shown in the table below. The 91-day bill had bid interest rates ranging from 25.9057% to 26.500%, with a weighted average rate of 26.1901%. For the 182-day bill, interest rates ranged between 27.0019% and 27.500 %, averaging 27.2911%. The 364-day bill recorded bid interest rates from 28.7333% to 29%, with a weighted average rate of 28.9706 %.

This week saw total bids of GH₵ 3,188.12 million for the 91-day bill, GH₵ 957.10 million for the 182-day bill, and GH₵ 276.32 million for the 364-day bill, all of which were fully accepted.

| Security |

Current Wk % |

Previous Wk % |

| 91-Day GoG Bill |

26.1901 |

25.9444 |

| 182-Day GoG Bill |

27.2911 |

27.0307 |

| 364-Day GoG Bill |

28.9706 |

28.7371 |

Source(s): Bank of Ghana

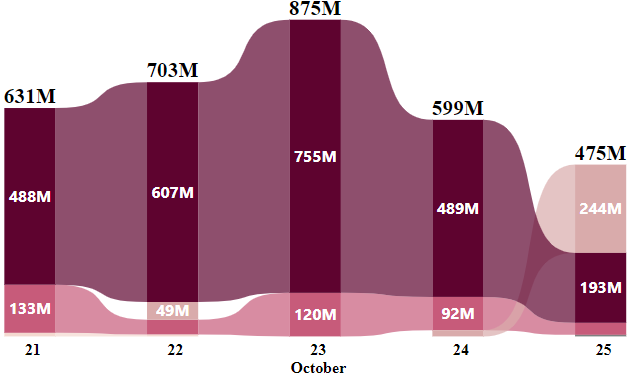

GHANA FIXED INCOME MARKET VOLUME TRADED

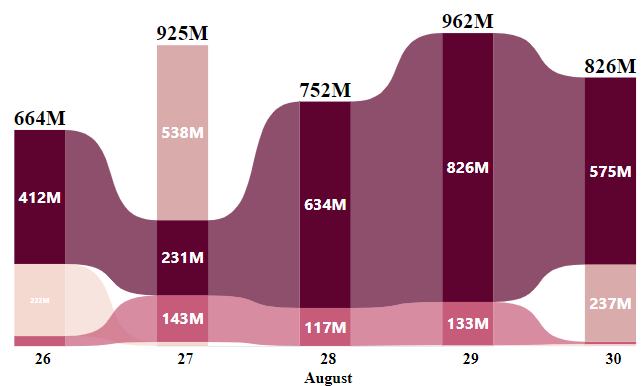

The Ghana Fixed Income Market closed the week with a total volume traded of GH₵ 3.28 billion. A total of 14,007 trades were made of which 99.59% were Treasury bills, and 0.27% were New GoG. Bonds and Notes.

Week’s Ghana Fixed Income Market Total Volume Traded

Starting at GH₵ 631 million on October 21, trading was primarily driven by Treasury Bills and newly issued Government of Ghana (GoG) Bonds and Notes. This volume rose to GH₵ 703 million on October 22, with Treasury Bills and Sell/Buy Back trades contributing significantly to the increase.

October 23 saw continued momentum, led by Treasury Bills and new GoG Bonds and Notes. However, trading volumes fell to GH₵ 599 million on October 24, still dominated by Treasury Bills. The week concluded with a more pronounced drop to GH₵ 475 million on October 25, where Sell/Buy Back trades and Treasury Bills were the primary contributors. Throughout the week, Treasury Bills consistently held the highest share of trading activity on the GFIM.

EQUITY MARKET

This week, trading on the local stock exchange reflected a subdued performance, with total share volume declining by 28.06% to 801,810 shares, down from last week’s 1,114,611 shares. Despite the lower volume, the total traded value rose by 10.05%, reaching GH₵ 12.89 million, indicating higher-value transactions. Market capitalization experienced a slight increase, closing at GH₵ 99.95 billion, up 0.56% from the previous week.

In terms of market indices, the GSE Composite Index (GSE-CI) closed at 4,369.03, showing a weekly loss of 0.5% and a monthly loss of 0.25%, but maintaining a strong year-to-date gain of 39.58%.

Meanwhile, the GSE Financial Stocks Index (GSE-FSI) also increased to 2,215.22 points, posting a slight weekly increase of 0.54%, a monthly rise of 1.13%, and a year-to-date gain of 16.49%.

| EQUITY MARKET MOST TRADED STOCKS | ||

| Ticker |

Traded Volume |

Price (GHS) |

| CAL |

490,435 |

0.26 |

| MTNGH |

201,437 |

2.16 |

| GLD |

28,172 |

427.96 |

| FML |

23,332 |

3.70 |

| RBGH |

18,342 |

0.66 |

Source(s): Ghana Stock Exchange

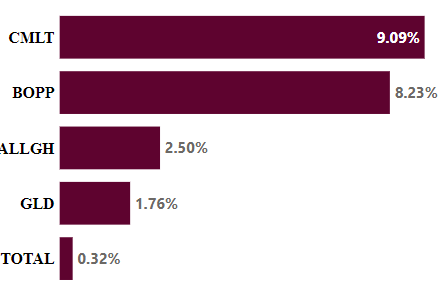

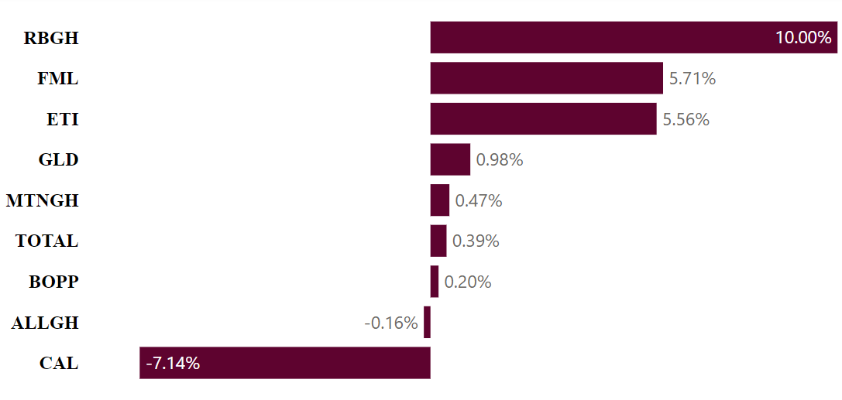

This week’s equity market activity was led by CalBank PLC (CAL), with the highest traded volume of 490,435 shares at a price of GH₵ 0.26. Scancom PLC (MTNGH) followed, trading 201,437 shares at GH₵ 2.16. NewGold ETF (GLD) saw a notable price point of GH₵ 427.96 with a volume of 28,172 shares, while Fan Milk Limited (FML) traded 23,332 shares at GH₵ 3.70. Republic Bank Ghana (RBGH) rounded out the top five, trading 18,342 shares at GH₵ 0.66.

| TOP PERFORMING AFRICAN STOCK INDICES YEAR-TO-DATE | |||

| Country |

Index |

Level |

YTD % |

| Zambia |

LuSE ASI |

16,242.06 |

▲50.00 |

| Ghana |

GSE-CI |

4,369.03 |

▲39.50 |

| Uganda |

USE ASI |

1,177.86 |

▲35.00 |

| Nigeria |

NGX ASI |

99,448.91 |

▲33.00 |

| Malawi |

MSE ASI |

145,230.00 |

▲30.90 |

Source(s): African Markets, AFX Kwayisi

COMMODITY MARKET

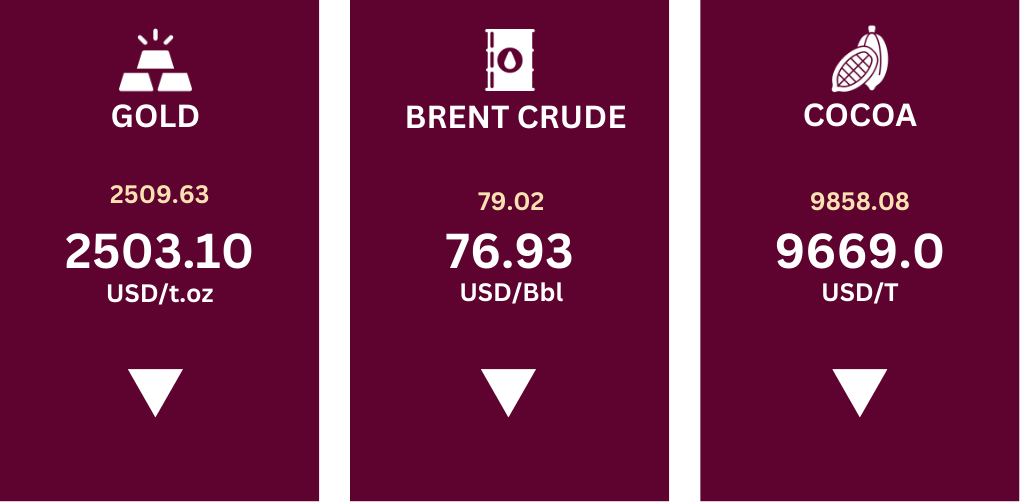

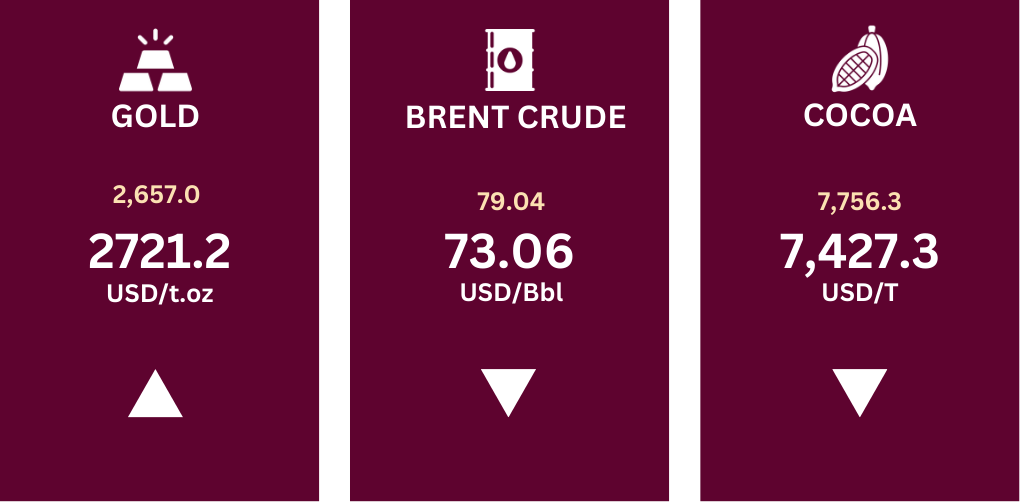

The commodities market experienced a divergent performance this week. Gold rose to $2,747.60 per ounce on Friday recovering from earlier profit-taking as geopolitical tensions in the Middle East and uncertainties surrounding the upcoming US election bolstered safe-haven demand.

Brent crude oil futures advanced 2.2% to settle at $76.06 per barrel on Friday, bouncing back from a two-day decline and securing a weekly gain of 4%. Investors are closely monitoring ongoing tensions in the Middle East, ceasefire negotiations, and the upcoming U.S. elections.

Source(s): Trading Economics

Cocoa futures dropped to close at $6,788.2 from $7,427.30 per tonne, reaching their lowest closing level since March, amid easing supply concerns in West Africa. Latest data showed bean arrivals at ports in Ivory Coast, the world’s top producer, have reached 192,804 tons from October 1 to October 20, up +12.9% from 170,794 MT shipped the same time last year, marking the first time in a year that arrivals are ahead of year-ago levels. Heavy rains in Ivory Coast earlier this month disrupted cocoa farming and transportation, but the easing wet weather is expected to improve pod harvesting and drying.

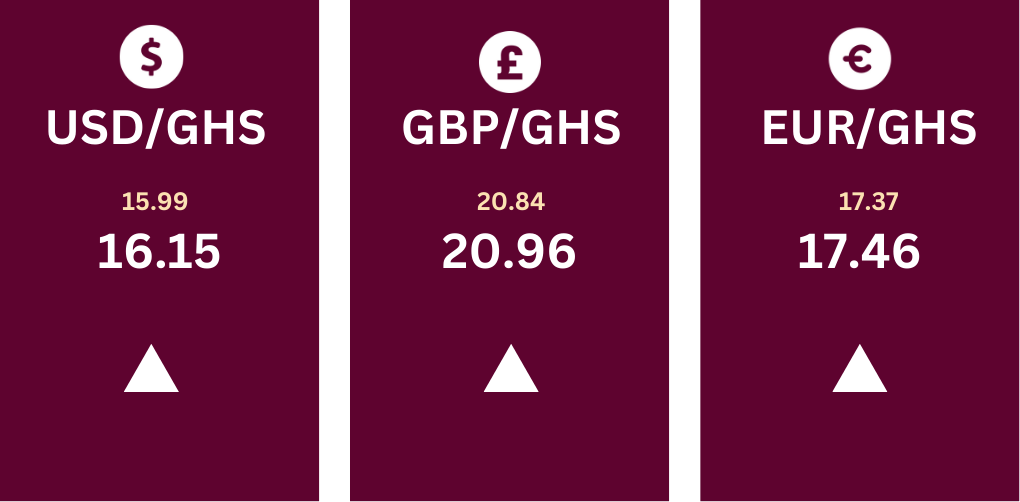

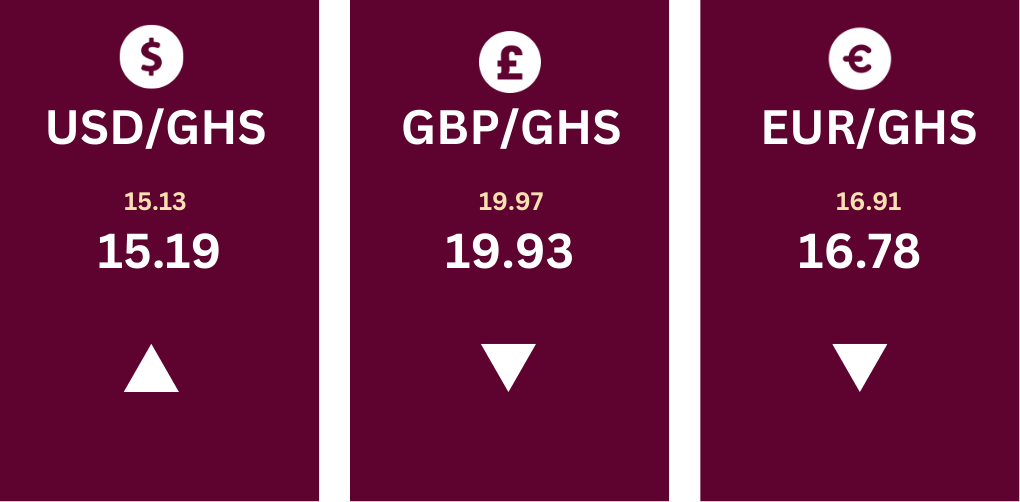

CURRENCY MARKET

The Ghanaian cedi has generally depreciated, experiencing slight declines across major foreign currencies. Against the US dollar, the USD/GHS rate moved from 15.99 to 16.15. Similarly, the cedi weakened slightly against the euro, with the EUR/GHS rate increasing from 17.37 to 17.46, while the GBP/GHS rate rose marginally from 20.84 to 20.96.