WEEKLY FINANCIAL MARKET REPORT AS OF 23RD AUGUST 2024

KEY HEADLINES

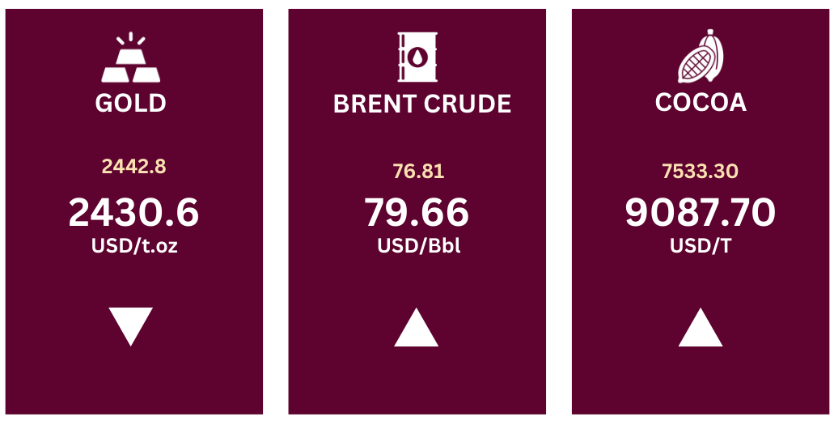

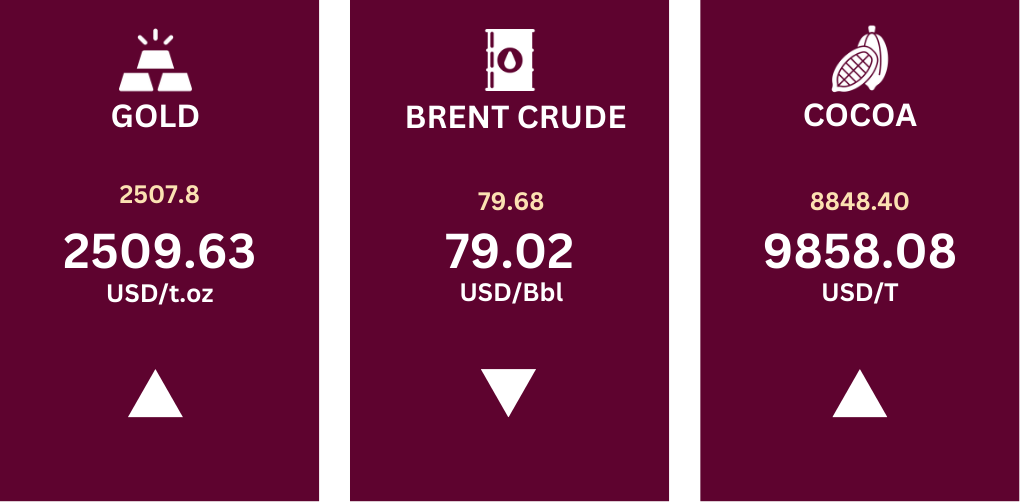

Gold records an all-time upturn value of $2,509.6 per troy ounce, on Monday, August 20.

Total shares traded on the Ghana Stock Exchange (GSE) plummeted by 88.85%, driven primarily by a sharp 90.54% contraction in Scancom PLC’s (MTNGH) trading volume compared to the previous week.

PRIMARY DEBT MARKET ISSUANCE WEEK

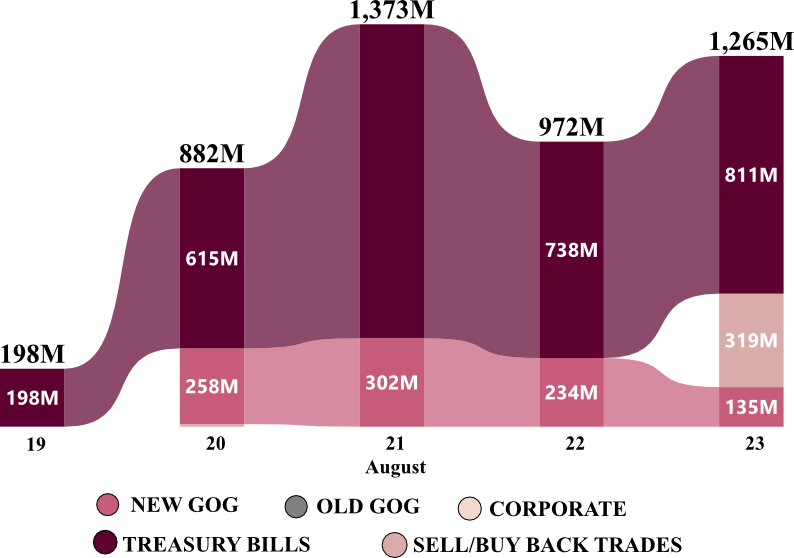

Interest rates on Government of Ghana Treasury Bills had a marginal downturn across all securities compared to the previous week. At the week’s auction, total bids received amounted to GH₵ 3,725.86 million for the 91-Day bill, GH₵ 1,251.99 million for the 182-Day bill, and GH₵ 252.74 million for the 364-Day bill, with all bids fully accepted.

| Security |

Range of Bid Rates (%) |

Current Wk % |

Previous Wk % |

| 91-Day GoG Bill |

23.3400 -23.3433 |

24.7895 |

24.8435 |

| 182-Day GoG Bill |

21.7610 – 23.5731 |

26.6854 |

26.7469 |

| 364-Day GoG Bill |

21.7800 – 21.7883 |

27.8135 |

27.8509 |

Source(s): Bank of Ghana

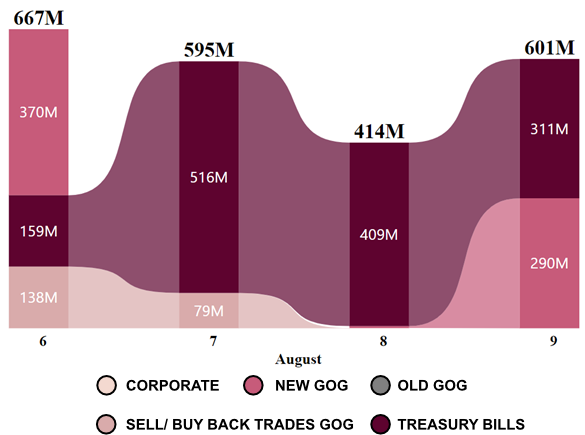

GHANA FIXED INCOME MARKET VOLUME TRADED

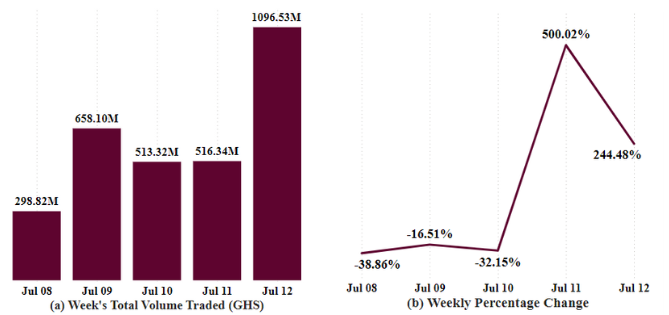

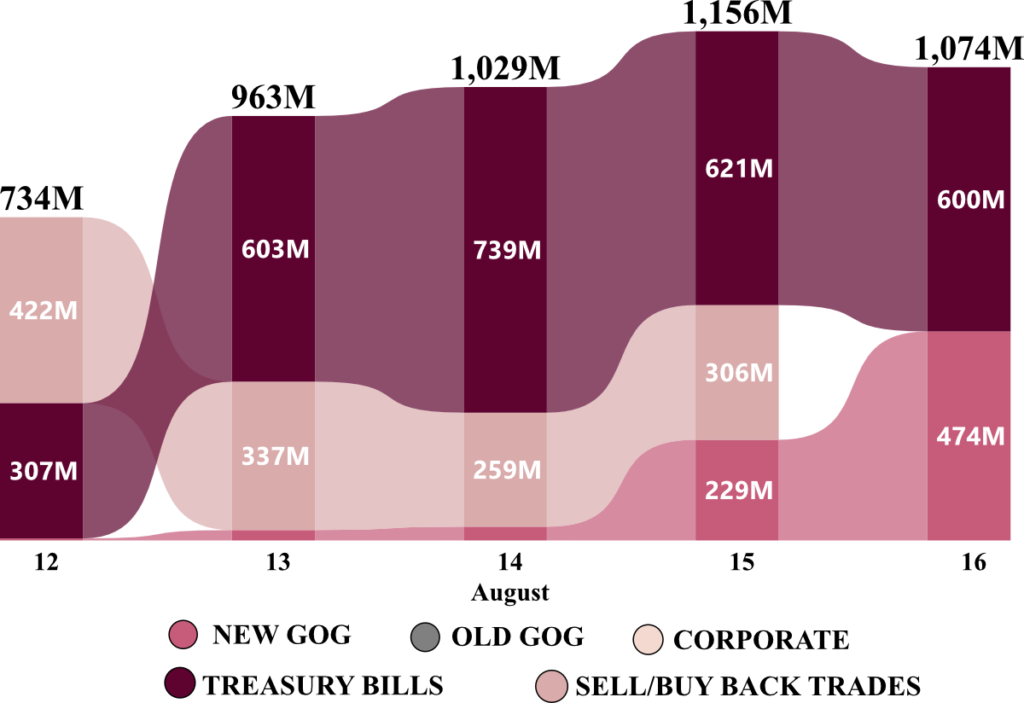

The Ghana Fixed Income Market (GFIM) closed the week with a total volume of GH₵ 4.69 billion from 6,137 trades. Treasury bills trades dominated the week’s trading activities by 96.42% and 3.44% for New GoG Notes & Bonds.

Week’s Ghana Fixed Income Market Total Volume Traded

The volume slightly took a downturn to GH₵ 972 million on August 22, again led by Treasury Bills, and ended at GH₵ 1,265 million on August 23, with significant contributions from Treasury Bills and Sell/ Buy Back Trades. Treasury Bills consistently dominated trading volumes throughout the week.

EQUITY MARKET

The week’s trading on the local bourse concluded with 1,993,860 shares exchanged, equivalent to GH₵ 6.82 million, bringing the market capitalisation to GH₵ 91.85 billion.

NewGold Issuer (GLD) emerged as the lead gainer, recording a 2.66% (from GH₵ 366.24 to GH₵ 376.00) uptick. The Trust Bank Limited (TBL) followed with a 1.22% gain, while TotalEnergies PLC (TOTAL) and GCB Bank PLC (GCB) posted modest gains of 0.24% and 0.17%, respectively.

On the downside, Scancom PLC (MTNGH) experienced a decline of 3.08% (from GH₵ 2.27 to GH₵ 2.20), but the most significant drop was seen in CalBank PLC (CAL), which dipped by 8.82% (from GH₵ 0.34 to GH₵ 0.31), indicating potential concerns among investors.

Week’s Equities Top Gainers & Laggards

Regarding market indices, the GSE Composite Index (GSE-CI) settled at 4,353.38, reflecting a weekly contraction of 1.96%, a monthly loss of 2.5%, but an overall year-to-date gain of 39.08%. The GSE Financial Stocks Index (GSE-FSI) ended at 2,118.06 points, making it a week loss of 0.22%, recording a monthly gain of 1.87% and a year-to-date return of 11.38%.

| EQUITY MARKET MOST TRADED STOCKS | ||

| Ticker | Traded Volume | Price (GHS) |

| MTNGH | 1,610,300 | 2.20 |

| SIC | 260,285 | 0.25 |

| CAL | 35,915 | 0.31 |

| ALLGH | 25,300 | 6.00 |

| ETI | 15,975 | 0.15 |

Source(s): Ghana Stock Exchange

COMMODITY MARKET

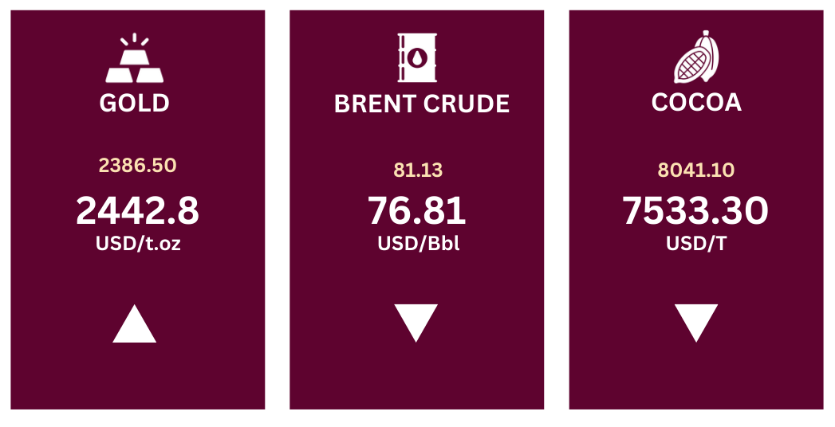

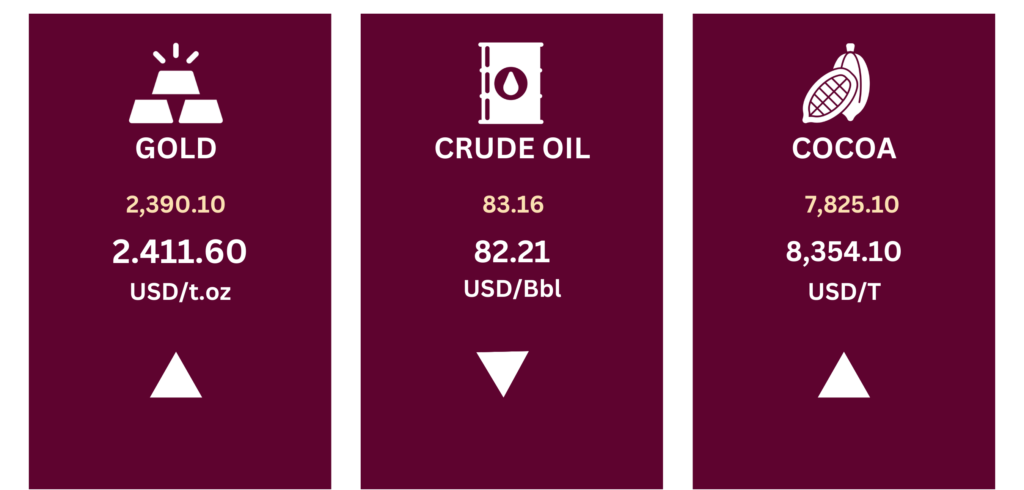

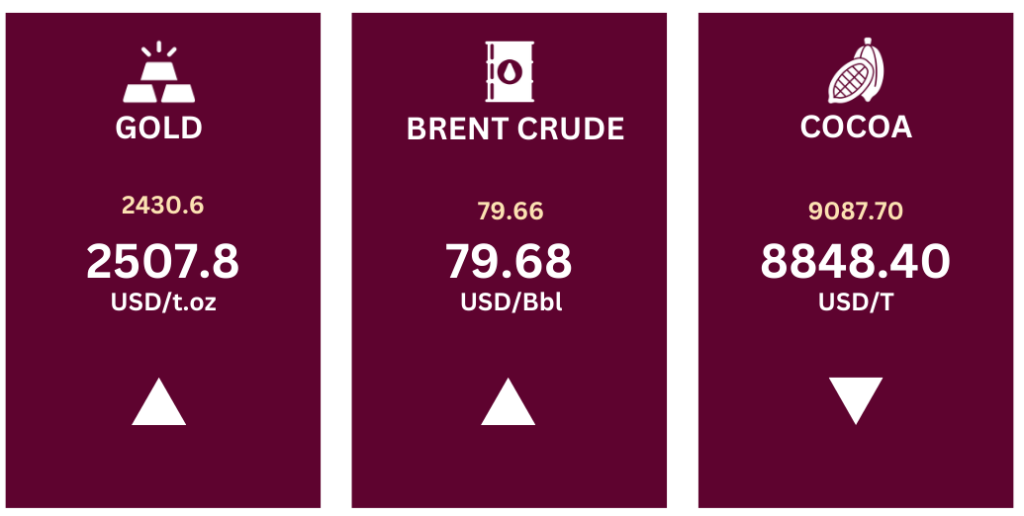

The commodities market experienced a divergent performance this week. Gold prices edged higher, increasing from US$ 2,507.8 to US$ 2,509.63 per troy ounce. The precious metal found support during afternoon trading, recovering to above $2,500 per ounce by Friday, maintaining proximity to its record highs as dovish signals from the Federal Reserve bolstered demand for non-yielding bullion assets.

In contrast, Brent crude prices softened, sliding from US$ 79.68 to US$ 79.02 per barrel. The decline in oil prices, exceeding 0.5% for the week, was driven by mounting concerns over weakening energy demand. This sentiment was reinforced by a slew of data indicating reduced fuel consumption, including the latest S&P PMI, which revealed a sharper-than-expected contraction in U.S. manufacturing activity in August.

Additionally, indicators of diminished fuel demand from major energy consumers, such as contractionary PMIs, declining industrial output, and ship-tracking data showing reduced fuel shipments to China in July, further pressured prices.

Source(s): Trading Economics

Cocoa prices surged, rising from US$ 8,848.40 to US$ 9,858.08 per ton, nearing their highest levels since mid-June fueled by ongoing concerns over constrained supply. Market apprehensions are centered on the potential impact of dry weather conditions in major West African-producing regions, which could significantly reduce global cocoa production.

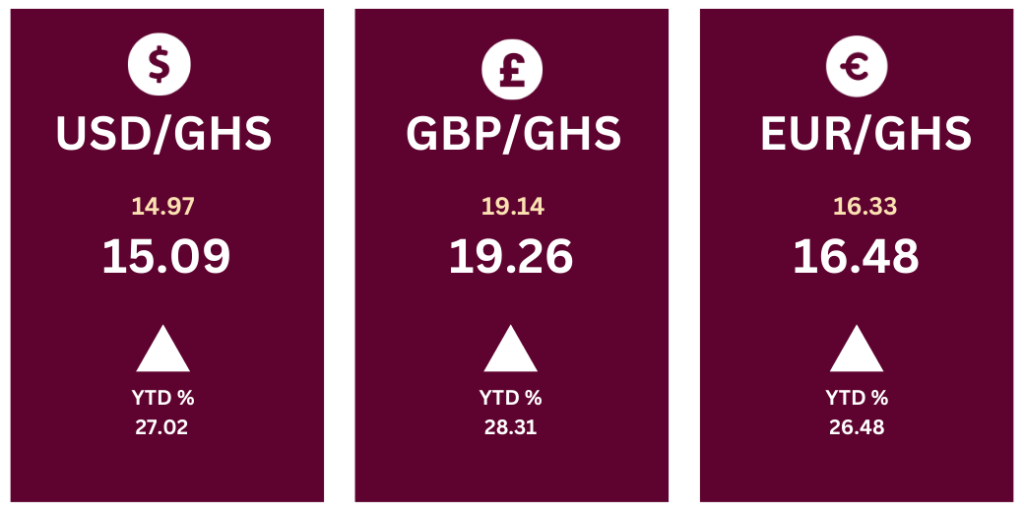

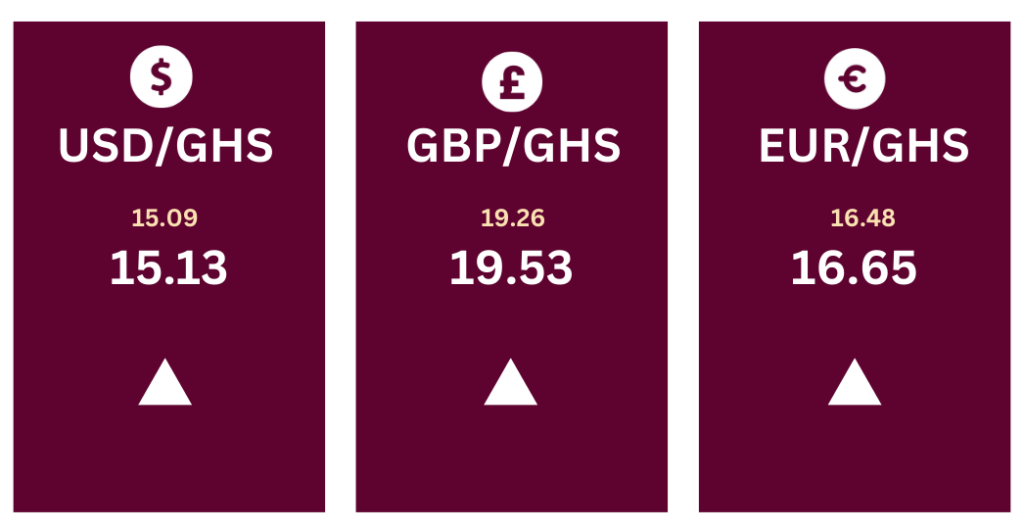

CURRENCY MARKET

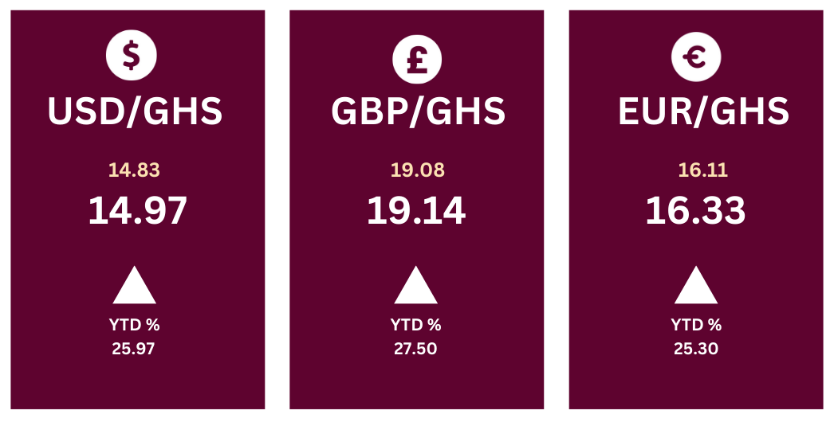

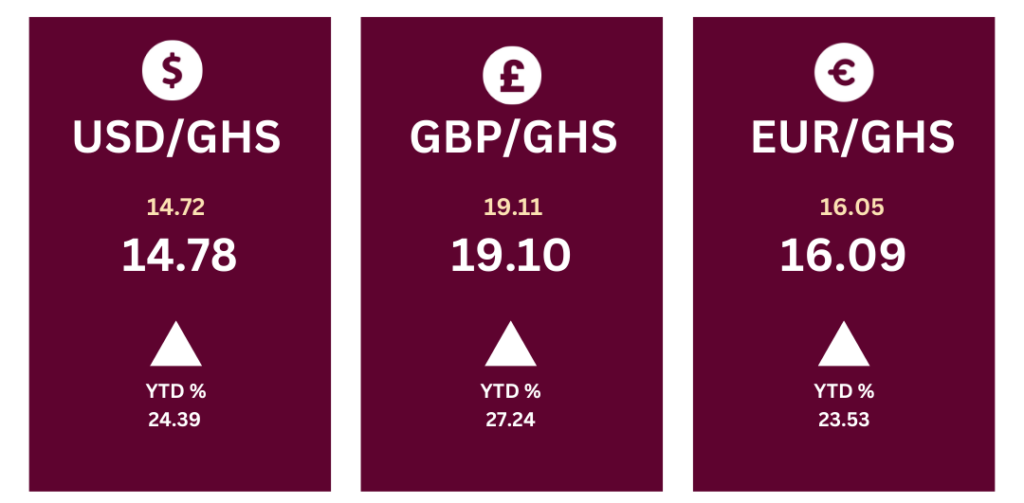

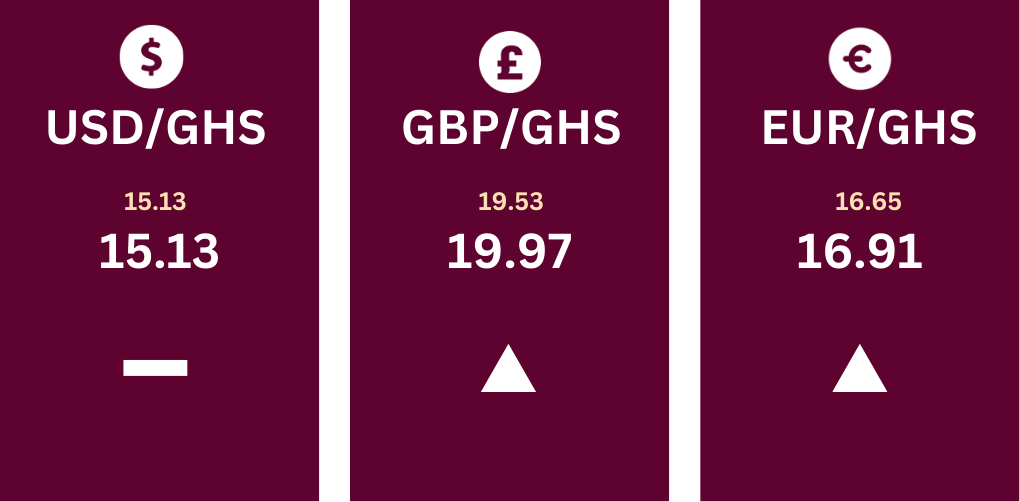

The exchange rates for the Ghanaian cedi (GHS) against major currencies exhibited mixed movements compared to the previous week. The USD/GHS rate held steady at GH₵ 15.13, showing no change. In contrast, both the British pound (GBP) and the euro (EUR) appreciated against the cedi, with GBP/GHS rising from GH₵ 19.53 to GH₵ 19.97, and EUR/GHS increasing from GH₵ 16.65 to GH₵ 16.91.

Source(s): Bank of Ghana

Source(s): Bank of Ghana

Source(s): Bank of Ghana