WEEKLY FINANCIAL MARKET REPORT AS OF 6TH SEPTEMBER 2024

KEY INSIGHTS

The 91-Day Treasury Bills saw a 54% increase in bids accepted, while the 182-Day Bills dropped by 45%, and the 364-Day Bills experienced a 4% decline in accepted bids compared to the previous week.

Ghana’s plans to increase the state-guaranteed price paid to cocoa farmers by nearly 45% for the upcoming season, is likely to boost production.

The OPEC+ (Organization of the Petroleum Exporting Countries) postponed its planned production increase of 180,000 barrels per day until December.

Ghana Fixed Income Market’s total volume traded reached GH₵ 3.2 billion, a 32% loss compared to the previous week.

PRIMARY DEBT MARKET ISSUANCE WEEK

The GoG Treasury Bill interest rates had a general upturn in all securities compared to the previous week. This week’s total bids received amounted to GH₵ 3,903.45 million for the 91-day bill, GH₵ 748.58 million for the 182-day bill, and GH₵ 197.11 million for the 364-day bill, with all bids fully accepted.

The range of bid interest rates for the 91-day bill was between 24.442% and 24.9668%, with a weighted average interest rate of 24.901%. For the 182-day bill, bid interest rates ranged from 26.7702% to 26.7959%, with a weighted average interest rate of 26.790%. The 364-day bill had a bid interest rate between 27.910% and 28.0574%, with a weighted average interest rate of 27.926%.

| Security | Current Wk % |

Previous Wk % |

| 91-Day GoG Bill |

24.9013 |

24.8896 |

| 182-Day GoG Bill |

26.7899 |

26.7890 |

| 364-Day GoG Bill |

27.9258 |

27.9100 |

Source(s): Bank of Ghana

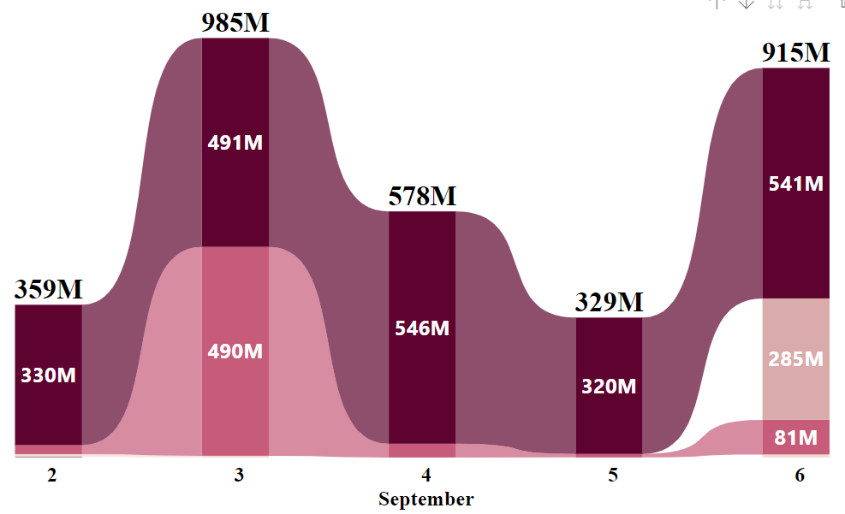

GHANA FIXED INCOME MARKET VOLUME TRADED

The Ghana Fixed Income Market (GFIM) closed the week with a total traded volume of GH₵ 3.2 billion across 5,586 transactions, with Treasury bills dominating 98.48% of the trades and New GoG Notes & Bonds accounting for 0.93%. From September 2 to September 6, 2024, trading volumes fluctuated across various securities. On September 2, the market recorded GH₵ 359 million in trades, primarily driven by Treasury bills. This increased to

GH₵ 985 million on September 3, supported by higher trading activity in both Treasury bills and New GoG Notes & Bonds. September 4 saw a downturn with GH₵ 578 million in volume, largely from Treasury Bills.

This was followed by another decline on September 5, where the volume saw a decrease to GH₵ 329 million, again led by Treasury Bills, and ended at GH₵ 915 million on September 6, with significant contributions from Treasury Bills and Sell/ Buy Back Trades.

EQUITY MARKET

This week’s trading on the local bourse concluded with 4,143,654 shares exchanged, equivalent to GH₵ 18.41 million, bringing the market capitalisation to GH₵ 91.8 billion.

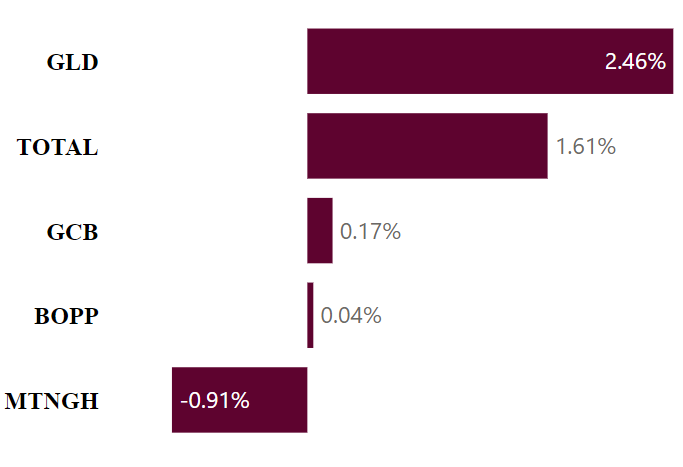

Week’s Equities Top Gainers & Laggard

In terms of market indices, the GSE Composite Index (GSE-CI) closed at 4,359.85, showing a weekly decline of 0.5% and a monthly drop of 2.32%, but maintaining a strong year-to-date gain of 38.58%. Meanwhile, the GSE Financial Stocks Index (GSE-FSI) remained steady at 2,118.52 points, posting a slight weekly increase of 0.02%, a monthly rise of 0.14%, and a year-to-date gain of 11.41%.

| EQUITY MARKET MOST TRADED STOCKS | ||

| Ticker |

Traded Volume |

Price (GHS) |

| MTNGH |

2,60,876 |

2.18 |

| EGH |

501,906 |

6.10 |

| SOGEGH |

362,260 |

0.25 |

| SIC |

342,365 |

6.15 |

| CAL |

210,724 |

0.31 |

Source(s): Ghana Stock Exchange

In the equity market, MTN Ghana (MTNGH) led trading activity with a volume of 2,260,876 shares exchanged for GHS 2.18 per share. Ecobank Ghana (EGH) followed with 501,906 shares traded at GHS 6.10. Société Generale Ghana (SOGEGH) recorded a volume of 362,260 shares at GHS 0.25, while SIC Insurance (SIC) traded 342,365 shares at GHS 6.15. CAL Bank (CAL) rounded out the top five most traded stocks with 210,724 shares at GHS 0.31 per share.

| TOP PERFORMING AFRICAN STOCK INDICES YEAR-TO-DATE | |||

| Country |

Index |

Level |

YTD % |

| Zambia |

LuSE ASI |

15,314.41 |

▲41.43 |

| Ghana |

GSE-CI |

4,337.92 |

▲38.58 |

| Malawi |

MSE ASI |

143,389.34 |

▲29.24 |

| Nigeria |

NGSE ASI |

96,433.53 |

▲28.97 |

| Uganda |

USE ASI |

1,058.42 |

▲21.31 |

Source(s): African Markets

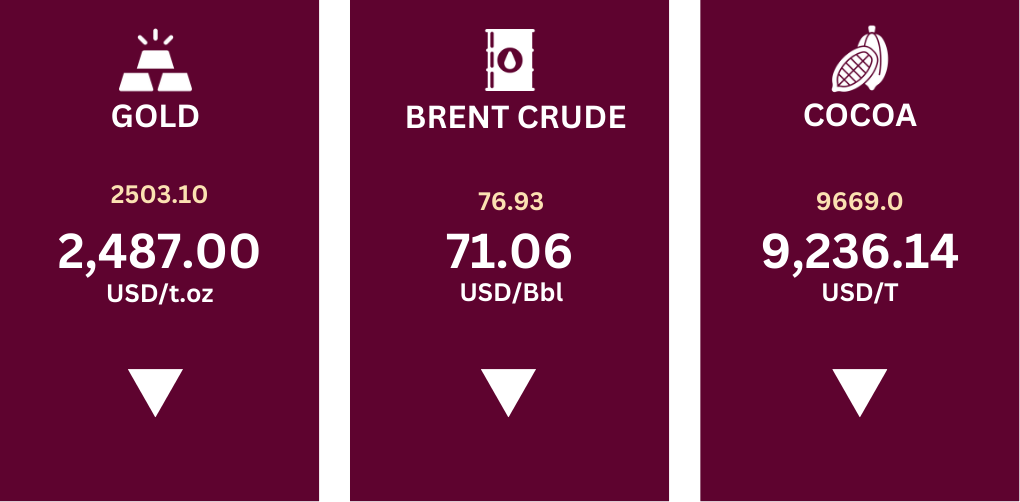

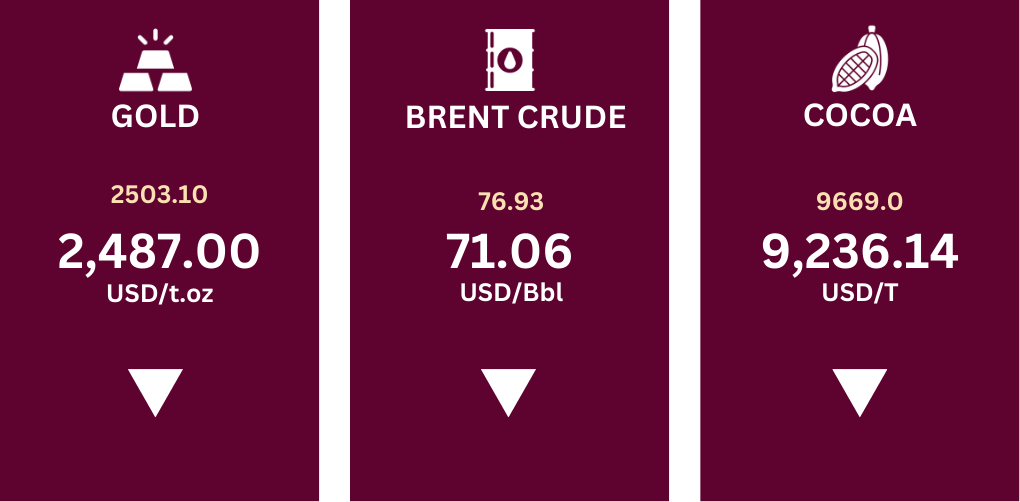

COMMODITY MARKET

The commodities market experienced a general dip in performance compared to the previous week. Gold prices dipped, decreasing from US$ 2,503.10 to US$ 2,487.10 per troy ounce.

Brent crude prices softened, sliding from US$ 76.93 to US$ 71.06 per barrel, the lowest since December 2021, as OPEC+ struggled to ease market concerns about global supply and demand. OPEC+ postponed its planned production increase of 180,000 barrels per day until December, which would have added about 2.2 million barrels per day to the market through the end of next year.

Source(s): Trading Economics

Cocoa prices were downturned, decreasing from US$ 9,669.0 to US$ 9236.14 per ton. Meanwhile, traders continued to weigh positive prospects for next season’s crop in the key producing region of West Africa, where anticipated rainfall is expected to benefit production. Additionally, Ghana’s plans to increase the state-guaranteed price paid to cocoa farmers by nearly 45% for the upcoming season, is likely to boost production.

CURRENCY MARKET

The Ghanaian cedi (GHS) continued to face downward pressure against major international currencies. The US dollar (USD), British pound (GBP), and euro (EUR) all appreciated relative to the cedi during the period under review.

Specifically, the USD/GHS exchange rate rose slightly from GH₵ 15.19 to GH₵ 15.35, a 5-year high since 2020. Similarly, the GBP/GHS rate increased from GH₵ 19.93 to GH₵ 20.15, and the EUR/GHS rate rose from GH₵ 16.78 to GH₵ 17.01. These movements suggest that the cedi is losing value compared to these key currencies.

Source(s): Bank of Ghana

DISCLAIMER: The information contained in this weekly update on the financial markets is intended for informational purposes only and should not be construed as financial, investment or other professional advice. The data are derived from internal and external sources that FFC Research finds reliable. FFC Research assumes no responsibility or liability for any actions taken based on the information contained in this report.

Research Analyst – Cedric Asante | Email: cedric.asante@firstfinancecompany.com