WEEKLY FINANCIAL MARKET REPORT AS OF 9TH AUGUST 2024

KEY HEADLINES

Bank of Ghana imposed sanctions on forty-seven (47) individuals and two-hundred and forty-five (245) business entities for persistent issuance of dub cheques (Bank of Ghana, 2024)

The FinTech Sector reports a 19.1% uptick in total transaction volume and a 37.3% uptick in total transaction value in Q2 compared to Q1. (Bank of Ghana, 2024)

Government plans to issue Treasury bills amounting to GH¢78,441.64 million for the period, July to September 2024 of which GH¢53,807.67 million is to rollover short-term maturities and the remaining GH¢24,633.97 million as fresh issuance to meet the Government’s financing requirements. (Bank of Ghana, 2024)

PRIMARY DEBT MARKET ISSUANCE WEEK

The Government of Ghana’s Treasury bills displayed minimal fluctuations in their yields over the recent period. The 91-day GoG bill showed a slight increase from 24.8246% to 24.8251%, while the 182-day GoG bill similarly increased from 26.7641% to 26.7642%. In contrast, the 364-day GoG bill experienced a marginal decline from 27.8578% to 27.8575%.

| Security | Current % | Previous % |

|

91-Day GoG Bill |

24.8251 |

24.8246 |

|

182-Day GoG Bill |

26.7642 |

26.7641 |

|

364-Day GoG Bill |

27.8575 |

27.8578 |

Source(s): Bank of Ghana

These insignificant shifts point to a rather steady short-term interest rate environment, suggesting that investors are still likely to retain interest in the government’s short-term debt instruments. The Government has set a target amount of GHS 4,968.00 million from the issue of the 91-Day, 182-Day, and 364-Day Treasury Bills for the next auction this coming week.

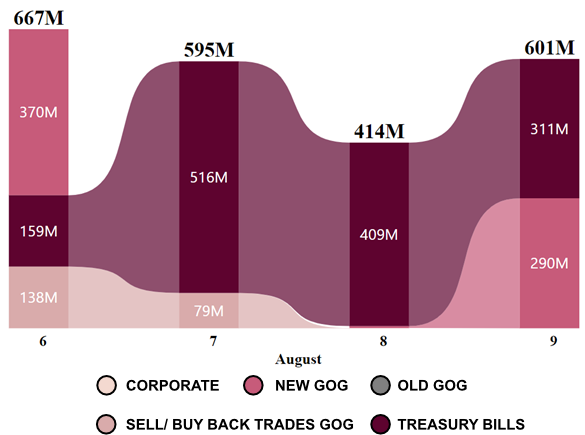

GHANA FIXED INCOME MARKET VOLUME TRADED

The Ghana Fixed Income Market concluded with a total volume traded of GHS 2.28 billion. A total of 5,949 trades were made of which 99.7% were Treasury bills, and 0.18% were New GoG Notes & Bonds.

On the 6th of August, the total market volume reached GHS 667 million, with Corporate Bonds contributing GHS 370 million and New GoG Notes GHS 159 million. The market experienced a slight

decline on the 7th to GHS 595 million, with Treasury Bills dominating the trades at GHS 516 million. On the 8th, the volume decreased further to GHS 414 million, where Treasury Bills again played a significant role, accounting for GHS 409 million of the total. However, by the 9th, the market volume recovered to GHS 601 million, with a notable balance between Treasury Bills (GHS 311 million) and Corporate Bonds (GHS 290 million).

EQUITY MARKET

This week’s trading on the local bourse concluded with a total volume of 578,885 shares exchanged, amounting to GHS 12,931,017.82, bringing the market capitalization to GHS 92.78 billion.

The stock market saw notable movements, with New Gold Issuer (GLD) leading the charge. GLD’s share price surged by GHS 5.30, closing at GHS 367.80, marking a significant gain. On the other hand, Scancom PLC (MTNGH) was the week’s underperformer, with its share price falling by GHS 0.12 to end at GHS 2.29.

Regarding market indices, the GSE Composite Index (GSE-CI) declined by 145.50 points to settle at 4,440.78, reflecting a weekly contraction of 3.17%, though it remains up 12.17% for the month and an impressive 41.87% year-to-date. Meanwhile, the GSE Financial Stocks Index (GSE-FSI) held steady at 2,115.52 points, recording a monthly gain of 1.33% and a year-to-date increase of 11.25%.

|

EQUITY MARKET MOST TRADED STOCKS |

||

|

Ticker |

Traded Volume |

Price (GHS) |

|

MTNGH |

278,190 |

2.29 |

|

CAL |

78,519 |

0.34 |

|

RBGH |

70,977 |

0.52 |

|

GLD |

32,560 |

367.80 |

|

ETI |

25,502 |

0.15 |

Source(s): Ghana Stock Exchange

|

TOP PERFORMING AFRICAN STOCK INDICES YEAR-TO-DATE |

|||

|

Country |

Index |

Level |

YTD % |

|

Ghana |

GSE-CI |

4,440.78 |

▲41.87 |

|

Zambia |

LuSE ASI |

14,378.52 |

▲32.79 |

|

Nigeria |

NGSE ASI |

98,592.12 |

▲31.85 |

|

Malawi |

MSE ASI |

134,526.12 |

▲21.25 |

|

Tanzania |

DSE ASI |

2,061.04 |

▲17.73 |

Source(s): AFX Kwayisi, African Markets

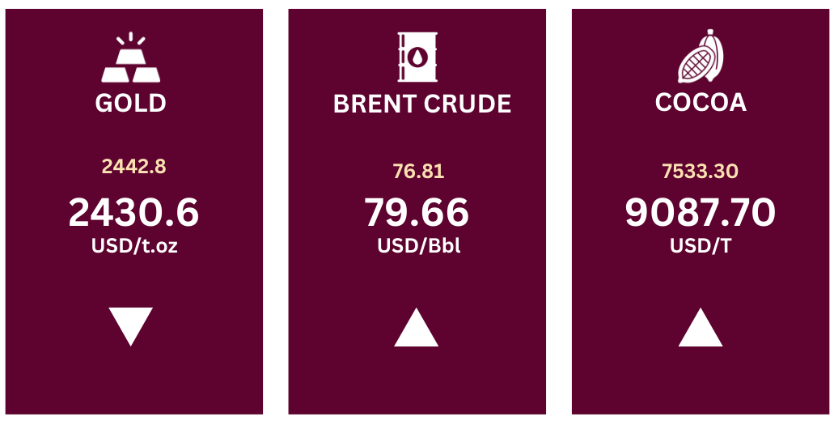

COMMODITY MARKET

The commodities market has shown varied performance. Gold prices slightly declined to US$ 2,430.6 from US$ 2,442.8 per troy ounce. Gold continues to gain support amid ongoing geopolitical uncertainties and the anticipation of a potential Federal Reserve rate cut. Additionally, while expectations for a Fed rate cut in September persist, investor sentiment has become more cautious. The market is now split on whether the Federal Reserve will opt for a 50 basis point reduction or a more conservative 25 basis point cut.

The price of Brent crude slightly increased from US$ 76.81 to US$ 79.66 per barrel of crude oil. This uptick was driven by positive economic data and indications from Federal Reserve officials that they might cut interest rates as soon as September, which alleviated some concerns about demand

Similarly, Cocoa prices increased from US$ 7,533.30 to US$ 9,087.70 per ton, the highest over seven weeks. In the short-term concerns persisted that increased rain in West Africa is making cocoa plantations more susceptible to disease and forcing farmers to buy expensive chemicals, allowing diseases such as Black Pod and Swollen shoot to resurface.

Source(s): Trading Economics

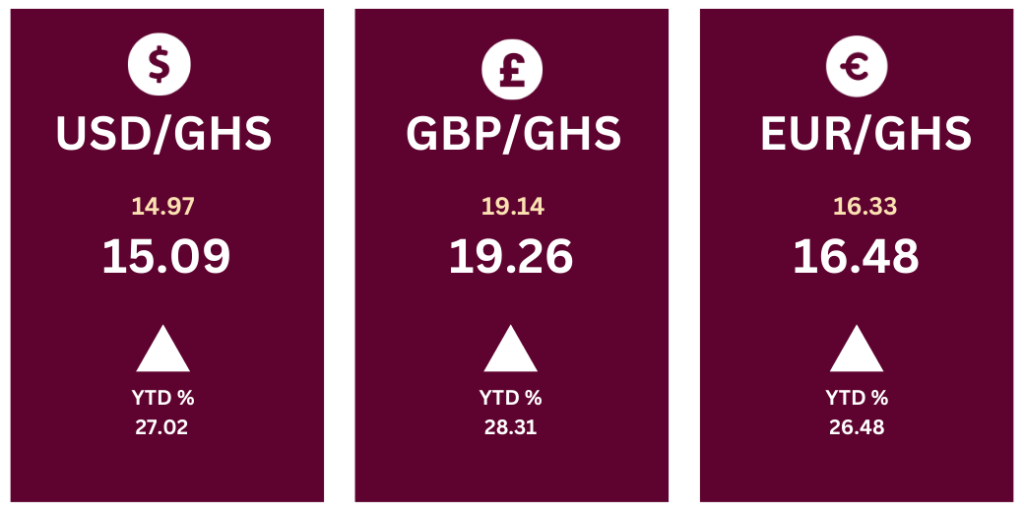

CURRENCY MARKET

The Ghanaian Cedi (GHS) has shown notable depreciation against major foreign currencies year-to-date (YTD). The exchange rate for USD/GHS has risen from GHS 14.97 (previous week) to GHS 15.09, with a 27.02% gain to the dollar YTD. Similarly, GBP/GHS increased from GHS 19.14 (previous week) to GHS 19.26, reflecting a 28.31% increase compared to the beginning of the year. The EUR/GHS exchange rate also climbed from GHS 16.33 (previous week) to GHS 16.48, indicating a 26.48% year-to-date gain for shared currency.

Source(s): Bank of Ghana

FINTECH SECTOR Q2 OVERVIEW

In Q2 2024, there were significant shifts in transaction values compared to Q1 2024, indicating growing consumer behaviour in digital financial services (Bank of Ghana, 2024). Agent-to-agent transactions underwent the most significant growth, rising by 33% from GHS 171.19 billion to GHS 228.03 billion, underscoring an increased reliance on peer-to-peer transfers. Third-party transactions also grew by 7%, reaching GHS 103.42 billion, suggesting expanded use of intermediaries or service providers. Bank-to-wallet (B2W) transactions increased by 11%, indicating a stronger preference for moving funds from traditional banks to digital wallets, which aligns with the broader trend towards digital financial inclusion.

Cash-out and cash-in transactions both saw a 14% increase, reflecting higher liquidity needs or greater consumer engagement within the mobile money ecosystem. However, Wallet-to-Bank (W2B) transactions decreased by 14%, declining from GHS 39.19 billion to GHS 33.88 billion, which may point to a preference for retaining funds within the digital wallet ecosystem rather than transferring them back to traditional banks.

These trends indicate that, despite the increasing popularity of digital financial services, particularly in peer-to-peer and bank-to-wallet transactions, there are segments of the market where consumer confidence or the perceived value of traditional banking services may be declining. This emphasizes the increasing significance of FinTech in the financial sector and suggests that there are both opportunities and challenges for companies that operate in this sector.