WEEKLY FINANCIAL MARKET REPORT AS OF 22ND NOVEMBER 2024

KEY HEADLINES & INSIGHTS

Ghana is clamping down on private pension fund managers who want to invest in offshore assets on concerns it could worsen pressure on its cedi currency (Reuters, 2024)

The Board of the International Monetary Fund (IMF) is set to meet in early December to review and potentially approve a $360 million disbursement to Ghana. (Citinewsroom, 2024)

Digital payment systems in Africa have grown by 37% in transaction volume over the past five years, reflecting a major shift in the continent’s financial ecosystem. (State of Inclusive Instant Payment Systems Report, 2024)

Ghana Fixed Income Market recorded a year-high total volume traded at GH₵ 1.96 billion, with GH₵ 1.68 billion attributed to Treasury bills.

PRIMARY DEBT MARKET ISSUANCE WEEK

This week, short-term Government of Ghana Treasury bills experienced varying interest rate increases compared to last week. The 91-Day GoG Bill rose by 22.32 basis points, reaching 27.1925% from 26.9693% last week, while the 182-Day GoG Bill increased by 20.08 basis points to 27.9884%. The 364-Day GoG Bill saw the largest rise, climbing 60.67 basis points to 29.8245%. These increases suggest a heightened demand for liquidity and adjustments in government borrowing rates.

| Security |

Current Wk % |

Previous Wk % |

| 91-Day GoG Bill |

27.1925 |

26.9693 |

| 182-Day GoG Bill |

27.9884 |

27.7876 |

| 364-Day GoG Bill |

29.8245 |

29.2178 |

Source(s): Bank of Ghana

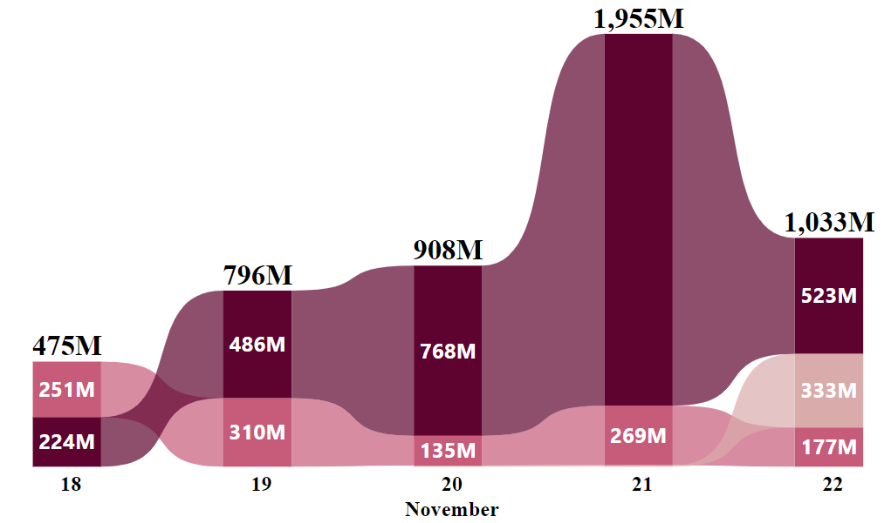

GHANA FIXED INCOME MARKET VOLUME TRADED

The Ghana Fixed Income Market closed the week with a total volume traded of GH₵ 5.17 billion compared to GH₵ 3.10 billion posted last week. A total of 7,269 trades were made of which 93.89% were Treasury bills, and 5.64% were attributed to New GoG (Government of Ghana) Notes & Bonds.

Week’s Ghana Fixed Income Market Total Volume Traded

Starting at GH₵ 475 million on November 18, trading was primarily driven by Treasury Bills and New GoG Notes & Bonds. This volume surged significantly to GH₵ 796 million on November 19, with Treasury Bills and New GoG Notes & Bonds contributing significantly to the increase.

November 20 saw the market continued uptick momentum, led by Treasury Bills. Subsequently, trading volumes inched up to GH₵ 1,955 million on November 21, still dominated by Treasury Bills and New GoG Notes & Bonds. The week concluded with a dip to GH₵ 1,033 million on November 22, where Sell/Buy Back trades and Treasury Bills were the primary contributors.

EQUITY MARKET

This week, trading on the local stock exchange booked a downturn performance, with total share volume declining by 12.19% to 1,252,403 shares, down from last week’s 1,426,300 shares. The total traded value also dipped by 56.78%, reaching GH₵ 3.44 million, indicating lower-value transactions. Market capitalization experienced a slight increase, closing at GH₵ 104.50 billion, up 0.29% from the previous week’s value of GH₵ 104.20 billion.

In terms of market indices, the GSE Composite Index (GSE-CI) closed at 4,665.35, showing a weekly gain of 0.15%, a monthly gain of 6.78%, and a strong year-to-date gain of 49.04%.

Moreover, the GSE Financial Stocks Index (GSE-FSI) also inched up to 2,325.64 points, posting a slight weekly increase of 0.43%, a monthly rise of 4.98%, and a year-to-date gain of 22.3%.

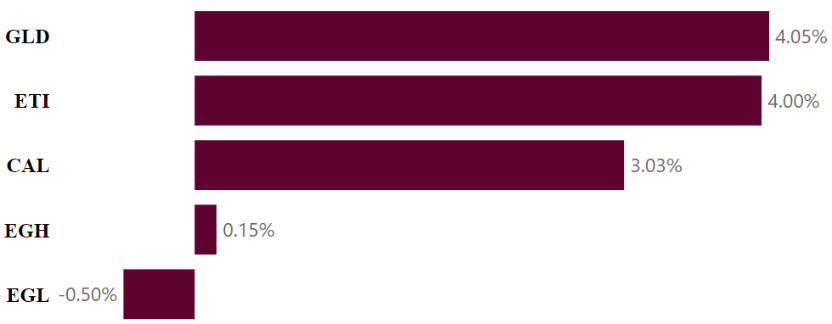

Week’s Equities Top Gainers & Laggards

| EQUITY MARKET MOST TRADED STOCKS | ||

| Ticker |

Traded Volume |

Price (GHS) |

| MTNGH |

909,998 |

2.36 |

| CAL |

105,417 |

0.34 |

| EGH |

102,979 |

6.50 |

| ETI |

85,113 |

0.26 |

| RBGH |

14,738 |

0.66 |

Source(s): Ghana Stock Exchange

This week, Scancom PLC (MTNGH) led the market with 909,998 shares traded at GHS 2.36, reflecting strong investor interest. CalBank PLC (CAL) and Ecobank Ghana (EGH) followed with 105,417 and 102,979 shares at GHS 0.34 and GHS 6.50, respectively, while Ecobank Transnational Incorporated (ETI) recorded 85,113 shares at GHS 0.26. Republic Bank PLC (RBGH) traded 14,738 shares at GHS 0.66, showing minimal activity. This week highlights investor focus on sector leaders and value stocks.

| TOP PERFORMING AFRICAN STOCK INDICES YEAR-TO-DATE | |||

| Country |

Index |

Level |

YTD % |

| Ghana |

GSE-CI |

4,665.35 |

▲49.04 |

| Zambia |

LuSE ASI |

15,828.65 |

▲46.18 |

| Malawi |

MSE ASI |

156,078.77 |

▲40.67 |

| Uganda |

USE ASI |

1,166.21 |

▲33.66 |

| Nigeria |

NGX ASI |

97,829.02 |

▲30.83 |

Source(s): African Markets

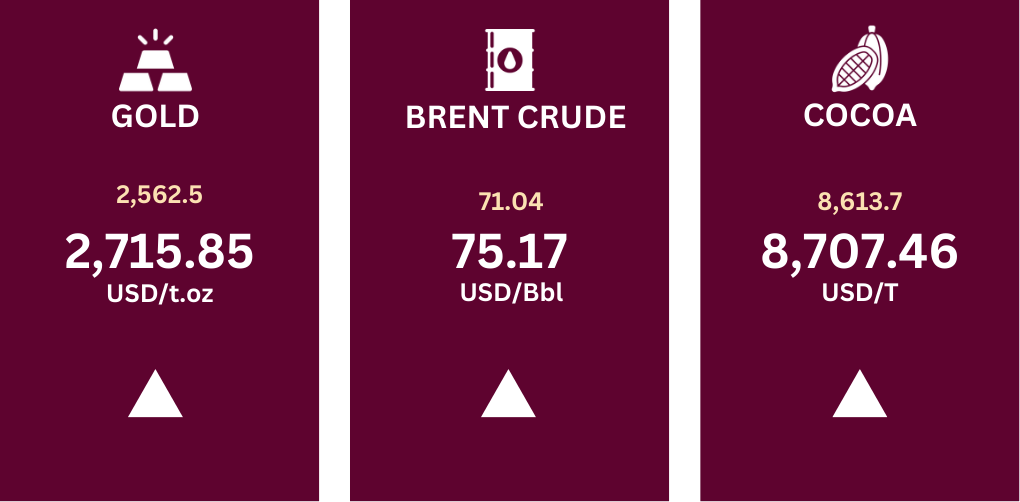

COMMODITY MARKET

The commodities market experienced a general upswing performance this week. Gold took an uptick to settle at $2,715.85 per ounce on Friday, rising for the fifth straight run, gained 5.9% compared to last week, as investors turned to safe-haven assets amid increasing geopolitical risks.

Brent crude oil futures inched up from $71.04 to settle at $75.17 per barrel on Friday, booking a weekly gain of 5.81%, attributed to intensifying conflict in Ukraine, which added a geopolitical risk premium to oil prices. Moscow ramped up its offensive after the US and UK allowed Ukraine to target deeper Russian territory with their missiles.

Source(s): Trading Economics

Cocoa futures surged to close at $8,707.46 from $8,613.7 per ton last week, reaching their highest level since early September amid mounting supply concerns. Dealers pointed to unfavourable weather in the Ivory Coast, the top cocoa producer, including the prospect of early dry Harmattan, winds this year, which could damage cocoa pods and dry out the soil, resulting in smaller beans.

CURRENCY MARKET

The exchange rates posted a downward trend compared to the previous week, with the Ghanaian cedi marginally appreciating against the major currencies. For USD/GHS, the rate decreased from 15.98 to 15.80, for GBP/GHS, it dropped from 20.17 to 19.77, and for EUR/GHS, it declined from 16.86 to 16.43. This suggests a strengthening of the cedi, possibly due to improved economic factors, increased foreign exchange inflows, or reduced demand for these currencies.

Source(s): Bank of Ghana

DISCLAIMER: The information contained in this weekly update on the financial markets is intended for informational purposes only and should not be construed as financial, investment or other professional advice. The data are derived from internal and external sources that FFC Research finds reliable. FFC Research assumes no responsibility or liability for any actions taken based on the information contained in this report.

Research Analyst – Cedric Asante | Email: cedric.asante@firstfinancecompany.com