WEEKLY FINANCIAL MARKET REPORT AS OF 15TH NOVEMBER 2024

KEY HEADLINES & INSIGHTS

Bank of Ghana Suspends CBG’s Forex Trading License for One Month in Bold Enforcement Move (Bank of Ghana, 2024)

Ghana has launched an ambitious Climate Prosperity Plan (CPP) at COP 29 in Baku, a roadmap set to address climate change while boosting economic prosperity. (Ministry of Finance, 2024)

China was Ghana’s leading source of investment destinations in the first half of 2024. The Far East country had the highest number of registered projects of 26. (Ghana Investment Promotion Centre, 2024)

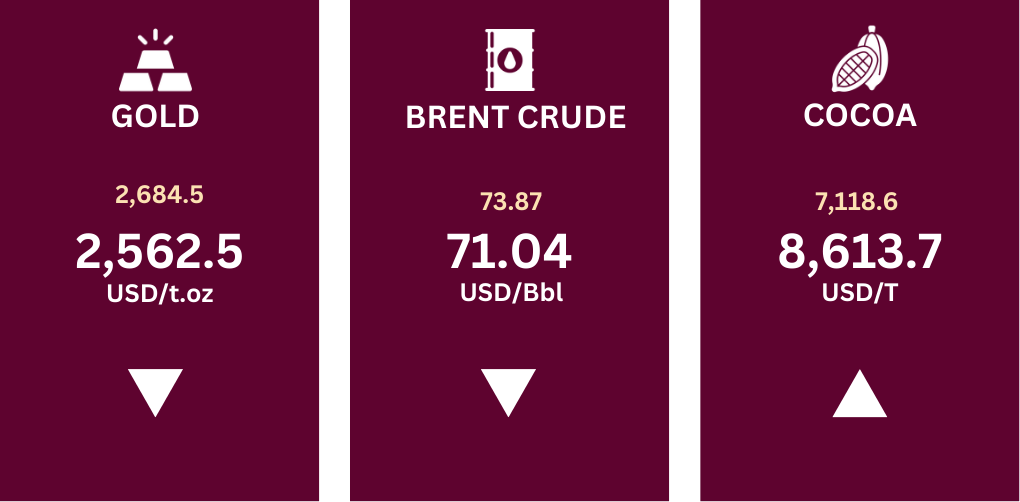

Cocoa futures soared, closing at $8,613.7 per ton, up from $7,118.6 last week. This sharp rise brings prices near the two-month high of $8,760 recorded on November 14th, fueled by ongoing concerns about tightening supply chains.

PRIMARY DEBT MARKET ISSUANCE WEEK

The interest rates on short-term Government of Ghana (GoG) Treasury Bills showed marginal increases across all maturities over the past week. The 91-Day GoG Bill rose by 14 basis points (bps) from 26.8293% to 26.9693%. Similarly, the 182-Day GoG Bill increased by 11 bps, climbing from 27.6763% to 27.7876%. The 364-Day GoG Bill recorded the smallest gain of 9 bps, rising from 29.1284% to 29.2178%. These incremental increases suggest a slight upward adjustment in yields, possibly reflecting market expectations of tighter liquidity or inflationary pressures.

| Security | Current Wk % | Previous Wk % |

| 91-Day GoG Bill | 26.9693 | 26.8293 |

| 182-Day GoG Bill | 27.7876 | 27.6763 |

| 364-Day GoG Bill | 29.2178 | 29.1284 |

Source(s): Bank of Ghana

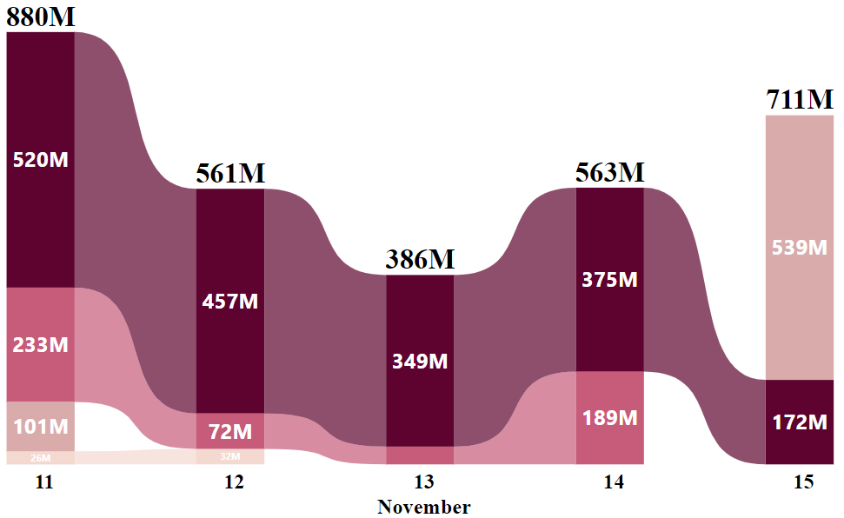

GHANA FIXED INCOME MARKET VOLUME TRADED

The Ghana Fixed Income Market closed the week with a total volume traded of GH₵ 3.10 billion. A total of 6,744 trades were made of which 94.29% were Treasury bills, and 4.64% were attributed to New GoG (Government of Ghana) Notes & Bonds.

Week’s Ghana Fixed Income Market Total Volume Traded

Starting at GH₵ 880 million on November 11, trading was primarily driven by Treasury Bills and New GoG Notes & Bonds. This volume dipped significantly to GH₵ 561 million on November 12, with Treasury Bills and New GoG Notes & Bonds contributing significantly to the increase.

November 13 saw the market continued downturn momentum, led by Treasury Bills. Subsequently, trading volumes rebounded to GH₵ 563 million on November 14, still dominated by Treasury Bills and New GoG Notes & Bonds. The week concluded with a more pronounced surge to GH₵ 711 million on November 15, where Sell/Buy Back trades and Treasury Bills were the primary contributors.

EQUITY MARKET

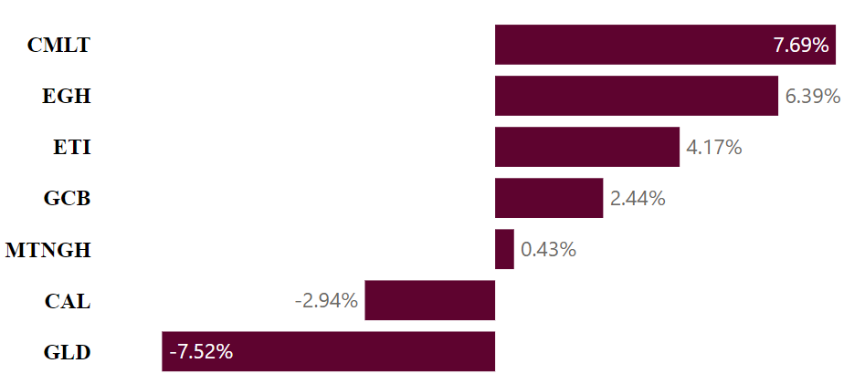

This week, trading on the local stock exchange booked a downturn performance, with total share volume declining by 42.41% to 1,426,300 shares, down from last week’s 2,478,901 shares. The total traded value also dipped by 38.25%, reaching GH₵ 7.96 million, indicating lower-value transactions. Market capitalization experienced a slight increase, closing at GH₵ 104.20 billion, up 0.42% from the previous week value of GH₵ 103.76 billion.

In terms of market indices, the GSE Composite Index (GSE-CI) closed at 4,658.30, showing a weekly gain of 0.63%, a monthly gain of 7.15%, and a strong year-to-date gain of 48.82%.

Week’s Equities Top Gainers & Laggards

Moreover, the GSE Financial Stocks Index (GSE-FSI) also inched up to 2,315.74 points, posting a slight weekly increase of 1.14%, a monthly rise of 5.1%, and a year-to-date gain of 21.78%.

| EQUITY MARKET MOST TRADED STOCKS | ||

| Ticker |

Traded Volume |

Price (GHS) |

| MTNGH |

658,800 |

2.36 |

| CAL |

326,674 |

0.33 |

| GCB |

284,720 |

6.30 |

| EGH |

100,127 |

6.49 |

| ETI |

28,771 |

0.25 |

Source(s): Ghana Stock Exchange

The equity market saw Scancom PLC (MTNGH) leading as the most traded stock with a volume of 658,800 shares at a price of GHS 2.36. CalBank (CAL) followed with 326,674 shares traded at GHS 0.33, while GCB Bank (GCB) recorded a trading volume of 284,720 shares at GHS 6.30. Ecobank Ghana (EGH) traded 100,127 shares at GHS 6.49, and Ecobank Transnational Incorporated (ETI) rounded out the list with 28,771 shares traded at GHS 0.25.

| TOP PERFORMING AFRICAN STOCK INDICES YEAR-TO-DATE | |||

| Country |

Index |

Level |

YTD % |

| Ghana |

GSE-CI |

4,658.30 |

▲48.82 |

| Zambia |

LuSE ASI |

15,984.74 |

▲47.62 |

| Malawi |

MSE ASI |

153,018.27 |

▲37.91 |

| Uganda |

USE ASI |

1,192.74 |

▲36.70 |

| Nigeria |

NGX ASI |

97,722.28 |

▲30.69 |

Source(s): African Markets

COMMODITY MARKET

The commodities market experienced a divergent performance this week. Gold took a downturn to settle at $2,562.50 per ounce on Friday heading for its worst weekly performance since June 2021 driven by a strong US dollar and reduced expectations for Federal Reserve rate cuts, which weakened the appeal of non-interest-bearing gold.

Brent crude oil futures dipped from $73.87 to settle at $71.04 per barrel on Friday, booking a weekly loss of 4%, attributed to pressure concerns over China’s waning demand and stronger US dollar. China’s crude processing dropped 4.6% in October, reflecting slower factory output and persistent demand issues.

Source(s): Trading Economics

Cocoa futures surged to close at $8,613.7 from $7,118.6 per ton last week, hovering close to a two-month high of $8,760 hit on November 14th, as concerns over tight supplies persisted. Cocoa prices have been rising significantly since early November due to adverse weather in West Africa, including below-average rainfall and above-average temperatures in areas of Ghana and Nigeria.

CURRENCY MARKET

The exchange rates posted a downward trend compared to the previous week, with the Ghanaian cedi marginally appreciating against the major currencies. For USD/GHS, the rate decreased from 16.35 to 15.98, for GBP/GHS, it dropped from 21.08 to 20.17, and for EUR/GHS, it declined from 17.50 to 16.86. This suggests a strengthening of the cedi, possibly due to improved economic factors, increased foreign exchange inflows, or reduced demand for these currencies.

Source(s): Bank of Ghana