WEEKLY FINANCIAL MARKET REPORT AS OF 30TH AUGUST 2024

KEY HEADLINES

The Ghana Stock Exchange Composite Index (GSE-CI) has seen an impressive 39.28% gain year-to-date.

Scancom PLC (MTNGH) records a 1,228,630 in shares traded, more than 300% of all other traded shares.

Total volume traded reached GH₵ 4.13 billion, with Treasury bills dominating the trades (98.66%).

OPEC (Organization of the Petroleum Exporting Countries) plans to increase production next quarter. (Yahoo Finance, 2024)

PRIMARY DEBT MARKET ISSUANCE WEEK

The GoG Treasury Bill interest rates had a general upturn in all securities compared to the previous week. This week’s total bids received amounted to GH₵ ¢ 2,532.03 million for the 91-day bill, GH₵ 1,357.13million for the 182-day bill, and GH₵ 205.23 million for the 364-day bill, with all bids fully accepted.

The range of bid rates for the 91-day bill was between 23.420% and 23.4319%, with a weighted average interest rate of 24.8896%. For the 182-day bill, bid rates ranged from 23.6200% to 23.6254%, with a weighted average interest rate of 26.7890%. The 364-day bill had a bid rate 21.8200%, with a weighted average interest rate of 27.9100%.

| Security | Current Wk % |

Previous Wk % |

|

91-Day GoG Bill |

24.8896 |

24.7895 |

|

182-Day GoG Bill |

26.7890 |

26.6854 |

|

364-Day GoG Bill |

27.9100 |

27.8135 |

Source(s): Bank of Ghana

![]()

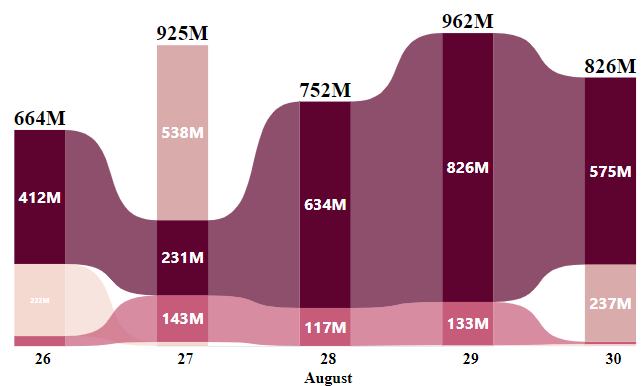

The Ghana Fixed Income Market closed the week with a total volume traded of GH₵ 4.13 billion. A total of 17,827 trades were made of which 98.66% were Treasury bills, and 1.05% were New GoG Notes & Bonds.

The trading activity on the Ghana Fixed Income Market (GFIM) from August 26 to August 30, 2024, shows fluctuating volumes across different security types. Trading began with GH₵ 664 million on August 26, with majority attributed to Treasury bills and Corporate Bonds. The volume then inched up to GH₵ 925 million on August 27, driven mainly by Sell/Buy Back Trades

August 28 saw a downturn with GH₵ 752 million in volume, largely from Treasury Bills.

The peak was on August 29, where the volume saw an uptick to GH₵ 962 million, again led by Treasury Bills, and ended at GH₵ 826 million on August 30, with significant contributions from Treasury Bills and Sell/ Buy Back Trades.

EQUITY MARKET

This week’s trading on the local bourse concluded with 1,155,073 shares exchanged, equivalent to GH₵ 3.15 million, bringing the market capitalisation to GH₵ 92 billion.

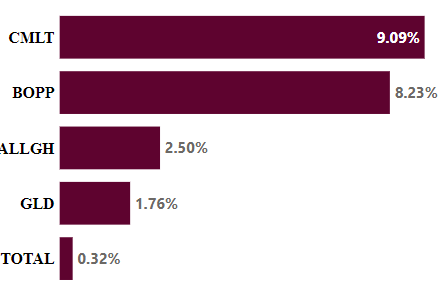

Week’s Equities Top Gainers

Regarding market indices, the GSE Composite Index (GSE-CI) settled at 4,359.85, reflecting a weekly gain of 0.15%, a monthly loss of 5.29%, but an overall year-to-date gain of 39.28%. Meanwhile, the GSE Financial Stocks Index (GSE-FSI) maintained it value at 2,118.06 points, recording a monthly gain of 0.77% and a year-to-date increase gain of 11.38%.

|

EQUITY MARKET MOST TRADED STOCKS |

||

|

Ticker |

Traded Volume |

Price (GHS) |

|

MTNGH |

1,228,630 |

2.20 |

|

GLD |

100,977 |

382.60 |

|

SIC |

44,426 |

0.25 |

|

ALLGH |

40,700 |

6.15 |

|

CAL |

37,666 |

0.31 |

Source(s): Ghana Stock Exchange

The recent trading data from the Ghana Stock Exchange highlights Scancom PLC (MTNGH) as the most actively traded stock, with over 1.2 million shares exchanged at GHS 2.20, reflecting strong investor confidence in the telecom giant. NewGold ETF (GLD), despite a lower volume of 100,977 shares, stands out with its high price of GHS 382.60, attracting those seeking a hedge against economic uncertainty.

SIC Insurance (SIC), trading at GHS 0.25, shows moderate interest in the insurance sector, possibly as a speculative play. Atlantic Lithium Ghana (ALLGH) traded 40,700 shares at GHS 6.15, suggesting market optimism about its prospects in the mining sector. CalBank (CAL) saw 37,666 shares traded at GHS 0.31, reflecting steady interest in the banking sector, with investors potentially viewing it as an affordable investment with growth potential. Overall, the diverse trading activity underscores a mix of growth opportunities and defensive plays in Ghana’s equity market.

COMMODITY MARKET

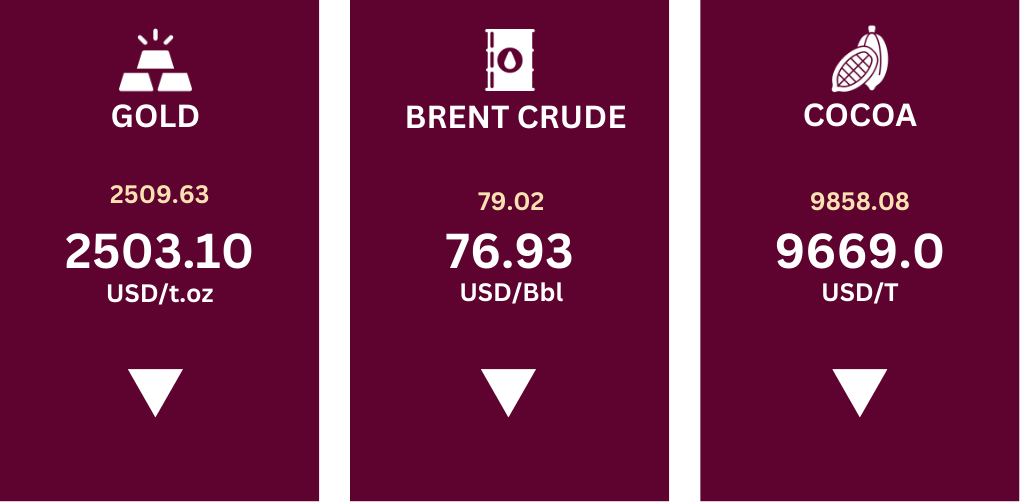

The commodities market experienced a general dip in performance compared to previous week. Gold prices inconsequentially dipped, decreasing from US$ 2,509.63 to US$ 2,503.10 per troy ounce., maintaining proximity to its record highs as dovish signals from the Federal Reserve bolstered demand for non-yielding bullion assets.

Brent crude prices softened, sliding from US$ 79.02 to US$ 76.93 per barrel. One significant driver of the price decrease is increased oil production by non-OPEC+ countries. These nations, including the United States, have ramped up their oil output. This surge in non-OPEC+ production has partially offset the supply curbs implemented by OPEC+ (the alliance of OPEC members and some non-OPEC producers)

Source(s): Trading Economics

Cocoa prices took a downturn, decreasing from US$ 9,858.0 to US$ 9,669.0 per ton, still nearing their highest levels since mid-June. This is due to a global supply shortage, investor speculation, and the impact on chocolate brands. The shortage stems from climate-induced crop damage in West Africa, while investor behavior has further driven prices upward.

CURRENCY MARKET

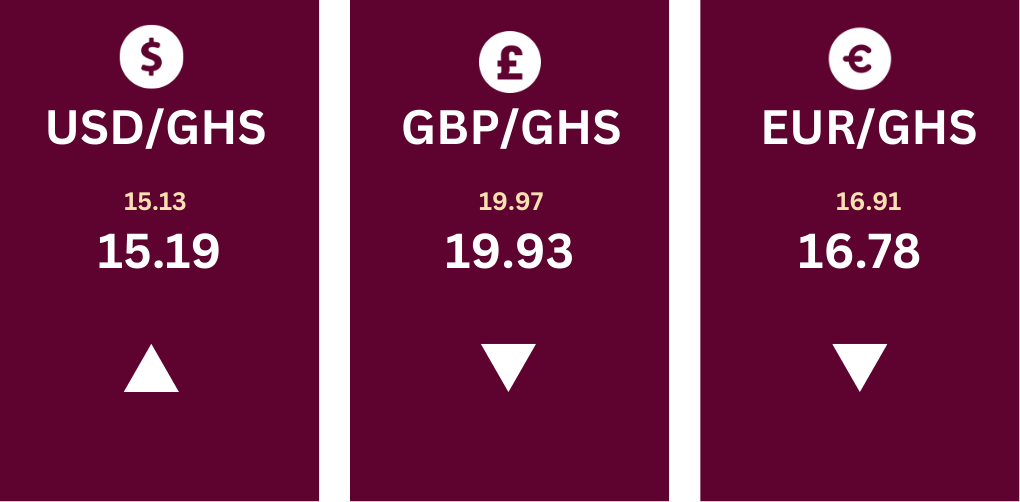

The exchange rates for the Ghanaian cedi (GHS) against major currencies exhibited mixed movements. The USD/GHS slightly increase from GH₵ 15.13 to GH₵ 15.19. Both the British pound (GBP) and the euro (EUR) slightly plummeted against the cedi, with GBP/GHS rising from GH₵ 19.97 to GH₵ 19.93, and EUR/GHS decreasing from GH₵ 16.91 to GH₵ 16.78.

Source(s): Bank of Ghana